Tax deed sales offer a unique pathway to real estate ownership, often at a fraction of market value, note Astoria Charm specialists. This guide demystifies the process, equipping investors with the knowledge to navigate its complexities, from due diligence to post-purchase management, and profit from tax deed acquisitions.

Understanding Tax Deeds: More Than Just a Discounted Property

Answer Capsule: A tax deed is a legal document granting property ownership to a buyer after a government foreclosure due to unpaid property taxes. Unlike tax liens, which represent a debt claim, a tax deed directly transfers the property title, often at a significantly reduced price. However, this opportunity comes with unique complexities, including potential title issues and redemption periods, demanding thorough understanding and due diligence.

A tax deed represents a government’s claim to a property due to unpaid taxes. When taxes are delinquent, the local government forecloses and sells the property at public auction. The winning bidder receives a tax deed, becoming the new legal owner. This process helps municipalities recover funds and offers investors discounted property.

Distinguishing a tax deed from a tax lien is crucial. A tax lien is a claim for unpaid taxes, granting the holder interest but not ownership. A tax deed, however, transfers actual property ownership after a government foreclosure. This distinction impacts both potential rewards and risks.

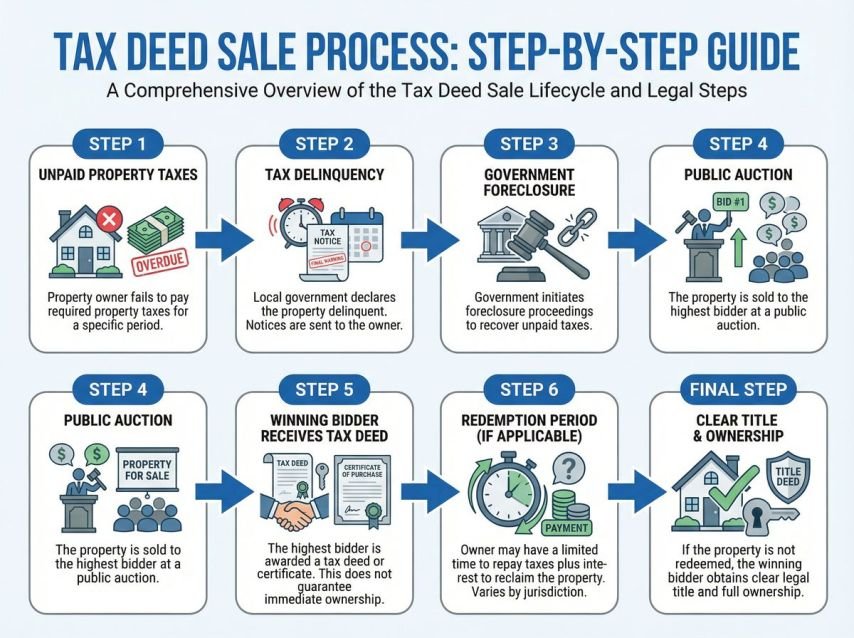

The Tax Deed Sale Process: A Step-by-Step Journey

Answer Capsule: The tax deed sale process typically begins with prolonged property tax delinquency, leading to government foreclosure and a public auction. Prospective buyers must research properties, register for auctions (online or in-person), and be prepared for immediate cash payment. Post-auction, redemption periods and title clearing procedures are critical steps before full ownership and potential profitability can be realized.

Acquiring a tax deed property follows a structured process, though timelines vary by jurisdiction. It begins with a property owner’s failure to pay taxes, leading to government foreclosure. This legal action declares the government’s intent to sell the property to satisfy outstanding tax debt.

Pre-auction, governments publish lists of properties for tax deed sales. Investors research these lists, verifying location, characteristics, and delinquent taxes. This initial research is vital for informed decisions and setting realistic bidding limits.

On auction day, tax deed sales occur in-person or online. Participants must register and be ready for immediate cash payment, typically within 24-72 hours. Effective bidding strategies are crucial to balance low acquisition costs against property value and renovation expenses, avoiding overpayment.

Post-auction, many jurisdictions have a redemption period, allowing former owners to reclaim property by paying taxes, penalties, and investor costs plus interest. This period varies by state. If redeemed, the investor receives their money back, often with interest, but loses the property. If not redeemed, the investor can secure a clear title, potentially through legal actions like a quiet title lawsuit.

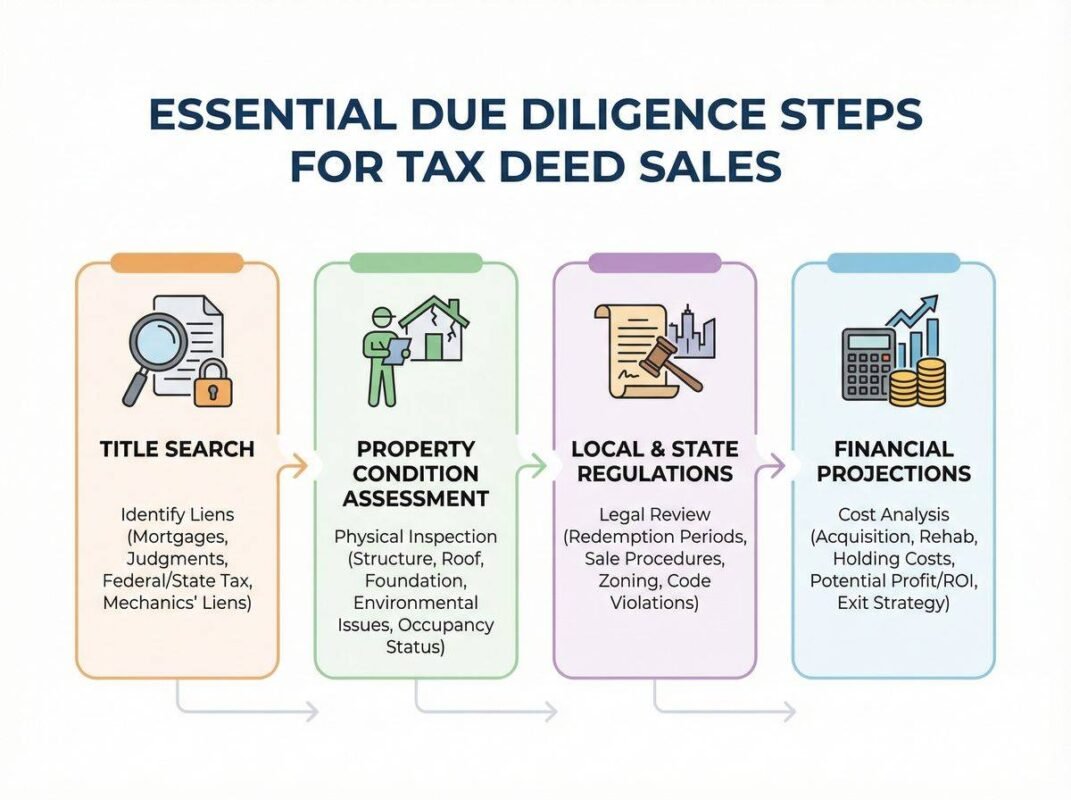

Essential Due Diligence: Uncovering Hidden Risks and Value

Answer Capsule: Thorough due diligence is paramount before participating in a tax deed sale to mitigate risks and accurately assess a property’s true value. This involves comprehensive title searches to identify hidden liens or encumbrances, physical inspection (if permitted) to evaluate property condition, and in-depth research into local and state regulations governing tax deed sales, including specific redemption period laws.

Unlike traditional real estate, tax deed sales operate on a “buyer beware” basis. Investors must uncover all potential issues before purchase, as neglecting due diligence can lead to unforeseen expenses, legal battles, or investment loss. Rigorous due diligence is therefore indispensable.

A comprehensive title search is crucial. Tax deed investing carries risks from existing liens or encumbrances, such as federal tax liens, which a tax deed may not extinguish. A qualified title company or attorney can identify these claims, revealing the property’s ownership history, mortgages, and judgments. Understanding these liabilities helps investors assess true costs and risks.

Property condition varies greatly, from minor disrepair to severe damage. Interior inspection before auction is often restricted, so investors use exterior visual inspections, satellite imagery, and local records. If interior access is possible, a professional inspection is recommended to uncover hidden defects and factor renovation costs into financial projections.

The legal framework for tax deed sales is complex and jurisdiction-specific. Investors must understand local regulations beyond redemption periods, including notice requirements, bidding procedures, payment deadlines, and clear title processes. Consulting a real estate attorney specializing in tax deeds is crucial for compliance and risk mitigation.

Post-Purchase Realities: Managing Challenges and Maximizing Returns

Answer Capsule: Acquiring a tax deed property often presents a new set of challenges beyond the auction itself, including potential issues with former occupants, property maintenance, and securing appropriate insurance. Proactive strategies for occupant removal, immediate property securing, and understanding specialized insurance options are crucial for minimizing liabilities and preparing the property for its intended use, whether resale or rental.

Winning a tax deed auction is just the beginning. The post-acquisition period involves practical and legal challenges that, if mishandled, can erode profitability. Efficiently addressing these realities is paramount to realizing the investment’s full potential.

Dealing with former occupants can be challenging. New owners may need to initiate formal eviction proceedings, adhering strictly to legal requirements to avoid delays and costs. Professionalism and understanding tenant rights are essential. A cash-for-keys incentive can sometimes expedite vacancy.

Upon securing possession, immediate steps include changing locks, boarding windows, and managing utilities. Neglecting these can lead to vandalism or liabilities. Ongoing maintenance is crucial; basic upkeep prevents deterioration, preserving value for quick flips. For rentals, a comprehensive maintenance plan attracts and retains tenants.

Securing appropriate insurance for tax deed properties is complex. Standard homeowner policies may not cover vacant or renovating properties, requiring specialized policies like vacant property or builder’s risk insurance. Activating utilities involves coordinating with local providers and budgeting for associated costs, a vital part of post-purchase planning.

Financing and Exit Strategies: Planning for Profitability

Answer Capsule: While many tax deed sales require cash, understanding alternative financing strategies and clear exit plans are vital for maximizing investment returns. Options like hard money loans or private financing can bridge funding gaps, while well-defined exit strategies—such as quick flipping, long-term rental, or rehab-and-sell—require careful market analysis and financial projections to ensure profitability and mitigate risks.

While tax deed auctions often require immediate cash, alternative financing strategies exist, making these opportunities accessible. A clear exit strategy is paramount; without a plan to monetize the property, even a discounted purchase can become a financial burden.

Beyond cash, investors can explore alternative financing. Hard money loans offer quick, short-term, asset-based capital for auctions, though with higher rates. Private money lenders provide flexible funding. Partnerships with cash-rich investors also allow resource pooling. Each option requires careful consideration of terms, risks, and financial goals.

Accurate financial projections are crucial for tax deed investing. Beyond the purchase price, investors must account for all costs: back taxes, penalties, legal fees, insurance, utility activation, and renovations. Overlooking these can eliminate profits. A comprehensive financial model should include acquisition, renovation, holding, marketing, and closing costs, plus a contingency fund for unexpected issues.

After acquiring and clearing title, investors choose an exit strategy: flipping (renovating for quick resale), renting (long-term income and appreciation), or holding (anticipating market appreciation). Each strategy has distinct risks and rewards, depending on investor goals and market conditions.

Frequently Asked Questions About Tax Deed Sales

Answer Capsule: This section addresses common inquiries regarding tax deed sales, clarifying key distinctions, risks, and practical considerations for potential investors. It covers the differences between tax liens and deeds, the inherent risks of such investments, the implications of redemption periods, the necessity of legal counsel, methods for locating sales, and whether this investment path suits beginners.

What is the difference between a tax lien and a tax deed?

A tax lien is a claim against a property for unpaid taxes, giving the holder the right to collect the debt plus interest. The lienholder does not own the property. A tax deed, conversely, transfers actual ownership of the property to the buyer after a government foreclosure due to chronic tax delinquency.

What are the risks of buying a tax deed property?

Key risks include potential title defects or hidden liens not extinguished by the sale, unknown property conditions requiring extensive repairs, the existence of redemption periods allowing former owners to reclaim the property, and the competitive nature of auctions leading to overpayment. Thorough due diligence is crucial to mitigate these risks.

What happens if the former owner redeems the property?

If a former owner redeems the property during the statutory redemption period, they pay the outstanding taxes, penalties, and often the investor’s purchase price plus interest. The investor typically receives their money back, along with any accrued interest, but loses ownership of the property.

Do I need a lawyer to buy a tax deed property?

While not always legally mandated, consulting a real estate attorney specializing in tax deeds is highly recommended. An attorney can assist with title searches, interpret complex local and state laws, navigate redemption periods, and facilitate the process of obtaining a clear title, significantly reducing legal risks.

How can I find tax deed sales?

Tax deed sales are typically advertised by local government entities, such as county tax collectors or clerks of court. Information can often be found on official county websites, in local newspapers, or through specialized online auction platforms dedicated to tax-defaulted properties.

Is tax deed investing a good idea for beginners?

Tax deed investing can be complex and carries significant risks, making it challenging for beginners. It requires substantial research, understanding of legal nuances, and often a significant cash outlay. Beginners should proceed with extreme caution, ideally with mentorship or professional guidance, and start with smaller, less risky investments.

References

- National Tax Lien Association (NTLA) – Annual Reports

- National Association of Counties (NACo) – Property Tax Collection and Enforcement Procedures by State

- Local County Tax Collector/Clerk of Court Websites

- Real Estate Attorneys specializing in Tax Deeds

- Reputable Real Estate Investment Forums and Educational Resources

Conclusion: Informed Investing for Real Estate Success

Tax deed investing offers a unique, potentially lucrative path to property ownership, but it’s complex and risky. Success requires rigorous due diligence, a deep understanding of legal frameworks, and meticulous planning for acquisition and post-purchase management. Informed decision-making and a proactive approach are key to transforming this venture into a strategic, profitable real estate investment.

Most Viewed