Purchasing a home for the first time is a significant financial and personal undertaking that involves a series of carefully managed steps, including assessing personal finances, understanding various mortgage products, navigating the property search, making a competitive offer, and completing the closing process, all of which contribute to a successful transition into homeownership, notes Tukwila Property Management Company.

Preparing Your Finances for a First Home Purchase

Preparing your finances for a first home purchase involves a thorough assessment of your credit score, managing debt-to-income ratio, accumulating a sufficient down payment, and setting aside funds for closing costs and unexpected expenses, ensuring you are financially ready for the significant investment of homeownership. This foundational step is crucial for determining affordability and securing favorable loan terms, ultimately shaping the entire homebuying experience.

Understanding Credit Scores and Debt-to-Income Ratio

Your credit score is a numerical representation of your creditworthiness, directly impacting the interest rates and loan terms you qualify for when seeking a mortgage. Lenders typically review scores from all three major credit bureaus—Experian, Equifax, and TransUnion—with higher scores generally leading to more favorable lending conditions. A good credit score, often considered to be 700 or above, demonstrates a history of responsible financial management, which is a key factor for mortgage approval. Conversely, a lower score may result in higher interest rates or require a larger down payment. The debt-to-income (DTI) ratio is another critical financial metric that lenders use to assess your ability to manage monthly payments and repay debts. It is calculated by dividing your total monthly debt payments by your gross monthly income. A DTI ratio of 36% or less is generally preferred by lenders, though some may approve ratios up to 43% or even 50% under certain circumstances, especially if you have a strong credit history or significant savings. Maintaining a low DTI ratio indicates that you have sufficient income to cover your existing debts and a new mortgage payment, reducing the perceived risk for lenders.

Down Payment and Savings Strategies

The down payment is the initial sum of money you pay towards the purchase of a home, and it significantly influences your mortgage terms and overall financial commitment. While a 20% down payment is often recommended to avoid private mortgage insurance (PMI), many loan programs, such as FHA loans, allow for much lower down payments, sometimes as little as 3.5%. VA and USDA loans may even offer 0% down payment options for eligible borrowers. Saving for a down payment requires disciplined financial planning, which can include setting up automated savings transfers, reducing discretionary spending, or exploring gift funds from family members. Beyond the down payment, it is essential to save for closing costs, which are fees associated with the mortgage and property transfer, typically ranging from 2% to 5% of the home’s purchase price. These costs can include loan origination fees, appraisal fees, title insurance, and legal fees. Additionally, first-time homebuyers should budget for moving expenses, initial home repairs or renovations, and an emergency fund to cover unexpected costs that may arise after moving in. Effective savings strategies ensure that you are not only able to afford the initial purchase but also maintain financial stability as a homeowner.

Navigating Mortgage Options and Pre-Approval

Navigating mortgage options and securing pre-approval is a critical step for first-time homebuyers, as it clarifies your borrowing capacity, identifies suitable loan types like conventional, FHA, VA, or USDA, and strengthens your offer to sellers by demonstrating financial readiness and commitment to purchasing a home.

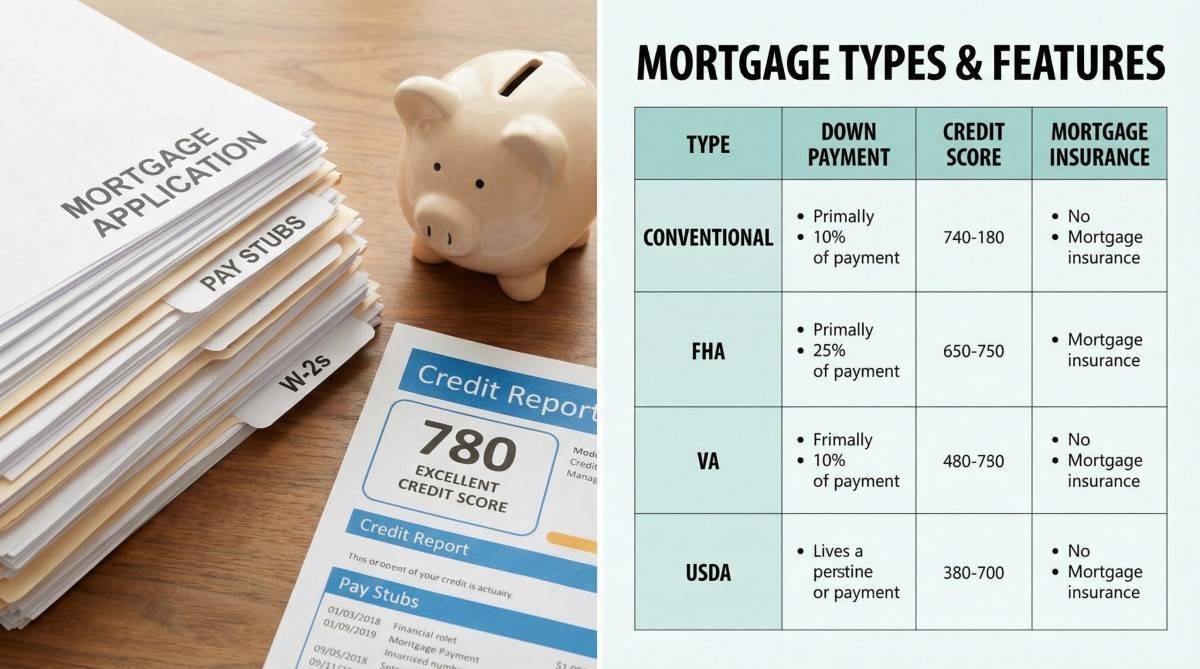

Types of Mortgages for First-Time Buyers

For first-time homebuyers, understanding the various mortgage types available is crucial for selecting a loan that best fits their financial situation and long-term goals. Conventional loans are the most common type, offered by private lenders and not insured by the government. They typically require a good credit score and can involve private mortgage insurance (PMI) if the down payment is less than 20%. FHA loans, insured by the Federal Housing Administration, are popular among first-time buyers due to their lower credit score requirements and down payments as low as 3.5%. However, they require both an upfront and annual mortgage insurance premium. VA loans, guaranteed by the U.S. Department of Veterans Affairs, are available to eligible service members, veterans, and surviving spouses, often requiring no down payment and no mortgage insurance. USDA loans, backed by the U.S. Department of Agriculture, are designed for low-to-moderate-income borrowers in eligible rural areas and also offer 0% down payment options. Each loan type has specific eligibility criteria, benefits, and drawbacks, making it essential to research and compare them thoroughly. Additionally, buyers must choose between fixed-rate mortgages, where the interest rate remains constant throughout the loan term, providing predictable monthly payments, and adjustable-rate mortgages (ARMs), where the interest rate can fluctuate after an initial fixed period, potentially leading to changes in monthly payments. The choice depends on market conditions, personal financial stability, and how long the buyer plans to stay in the home.

The Importance of Mortgage Pre-Approval

Obtaining a mortgage pre-approval is a pivotal step for first-time homebuyers, as it provides a clear understanding of how much a lender is willing to loan, thereby establishing a realistic budget for home shopping. A pre-approval is a conditional commitment from a lender, based on a review of your financial information, including income, assets, and credit history. It differs from a pre-qualification, which is merely an estimate based on self-reported information. With a pre-approval letter in hand, buyers demonstrate to sellers that they are serious and financially capable, which can be a significant advantage in a competitive housing market. The pre-approval process typically involves submitting financial documents such as pay stubs, bank statements, tax returns, and employment verification. This step not only streamlines the home search by narrowing down options to affordable properties but also identifies any potential financial issues that need to be addressed before making an offer. Furthermore, it allows buyers to compare loan offers from different lenders, ensuring they secure the most favorable interest rates and terms available.

Finding Your Home and Making a Competitive Offer

Finding your ideal home and crafting a competitive offer requires strategic planning, including working with an experienced real estate agent, understanding local market conditions, and structuring an offer that stands out while protecting your interests through contingencies, ultimately leading to a successful home acquisition.

Partnering with a Real Estate Agent

Partnering with a knowledgeable and experienced real estate agent is invaluable for first-time homebuyers, as they serve as a crucial guide through the complexities of the housing market. A good agent possesses in-depth local market expertise, including neighborhood insights, property values, and upcoming developments, which can significantly influence purchasing decisions. They assist in identifying properties that align with your budget, preferences, and pre-approval limits, often having access to listings before they become widely public. Beyond property identification, agents are skilled negotiators, advocating on your behalf to secure the best possible price and terms. They also help in navigating the intricate paperwork, disclosures, and legal aspects of a real estate transaction, ensuring all processes comply with local regulations. When selecting an agent, consider their experience with first-time buyers, communication style, and track record. Interviewing multiple agents and checking references can help you find a professional who understands your needs and can effectively represent your interests throughout the homebuying journey.

Crafting a Strong Purchase Offer

Crafting a strong purchase offer is essential, especially in a competitive real estate market, to increase the likelihood of seller acceptance while protecting your interests as a buyer. A comprehensive offer typically includes the proposed purchase price, a good-faith earnest money deposit, and crucial contingencies. Common contingencies include a home inspection contingency, allowing you to withdraw the offer or renegotiate if significant issues are found during the inspection, and an appraisal contingency, which protects you if the home appraises for less than the offer price. A financing contingency ensures you are not obligated to purchase if your mortgage loan falls through. To make an offer more appealing, consider offering a competitive price based on comparable sales in the area, minimizing contingencies if comfortable with the risks, or offering a flexible closing date that suits the seller. Your real estate agent will play a vital role in advising on market conditions, helping you structure an offer that balances attractiveness to the seller with necessary protections for you, and negotiating counteroffers to achieve a mutually agreeable outcome.

The Home Inspection and Closing Process

The home inspection and closing process are the final, crucial stages of buying a home, where a professional evaluation of the property’s condition ensures no major issues exist, and all legal and financial documents are meticulously reviewed and signed, culminating in the official transfer of ownership and receipt of keys.

What to Expect from a Home Inspection

After your offer is accepted, a professional home inspection is a critical step to evaluate the property’s condition and identify any potential issues before finalizing the purchase. A certified home inspector will thoroughly examine the home’s structural integrity, foundation, roof, HVAC systems, plumbing, electrical systems, and appliances. The inspection aims to uncover significant defects, safety hazards, or areas requiring major repairs that might not be apparent during a casual viewing. It is highly recommended that first-time homebuyers attend the inspection with their real estate agent, as this provides an opportunity to ask questions, gain a deeper understanding of the home’s condition, and learn about its various systems. Following the inspection, the inspector will provide a detailed report outlining their findings. Based on this report, buyers can negotiate with the seller for repairs, credits, or a reduction in the purchase price, or even withdraw their offer if the issues are too extensive or costly. This contingency protects the buyer from unforeseen expenses and ensures they are making an informed decision about their investment.

Understanding the Closing Day Procedures

Closing day marks the culmination of the homebuying process, where ownership of the property is officially transferred from the seller to the buyer. This day involves signing numerous legal and financial documents, and it is essential for first-time homebuyers to understand each step. Prior to closing, a final walkthrough of the property is typically conducted to ensure that any agreed-upon repairs have been completed and that the home is in the expected condition. At the closing table, which may be attended by the buyer, seller, real estate agents, and legal representatives, documents such as the promissory note, mortgage deed, and disclosure statements are signed. Buyers will also be responsible for paying closing costs, which can include loan origination fees, title insurance, escrow fees, and property taxes, among others. These costs are usually outlined in the Loan Estimate and Closing Disclosure provided by the lender. It is crucial to review these documents carefully and ask questions if anything is unclear. Once all documents are signed and funds are disbursed, the buyer receives the keys to their new home, officially becoming a homeowner.

First-Time Homebuyer Programs and Assistance

First-time homebuyer programs and assistance initiatives are designed to make homeownership more accessible by offering financial aid such as grants, low-interest loans, or down payment assistance, reducing upfront costs and easing the financial burden for eligible individuals embarking on their initial property purchase.

State and Local Assistance Programs

Many state and local governments offer a variety of programs specifically designed to assist first-time homebuyers, making homeownership more attainable. These programs often come in the form of down payment assistance (DPA), which can be grants that do not need to be repaid, or low-interest loans that are deferred or forgivable under certain conditions. Some programs also provide closing cost assistance, helping to reduce the upfront financial burden associated with purchasing a home. Eligibility for these programs typically depends on factors such as income limits, credit score requirements, and the location of the property. For instance, some programs might target specific professions, like teachers or first responders, or aim to revitalize certain neighborhoods. It is advisable for prospective buyers to research programs available in their specific state, county, or city, as offerings can vary significantly. Housing finance agencies (HFAs) at the state level are excellent resources for discovering these opportunities, often providing comprehensive lists and eligibility criteria. Engaging with a HUD-approved housing counseling agency can also provide personalized guidance on navigating these programs and understanding their benefits.

Federal Loan Programs and Benefits

Beyond state and local initiatives, several federal loan programs offer significant benefits to first-time homebuyers. The Federal Housing Administration (FHA) loan program is particularly popular, requiring a lower minimum down payment (as low as 3.5%) and more lenient credit score criteria compared to conventional loans. These loans are insured by the government, which allows lenders to offer more flexible terms. The U.S. Department of Veterans Affairs (VA) loan program provides a powerful benefit to eligible service members, veterans, and surviving spouses, often requiring no down payment and no private mortgage insurance. Similarly, the U.S. Department of Agriculture (USDA) loan program targets rural and suburban homebuyers, offering 0% down payment options for eligible properties and borrowers. These federal programs are instrumental in making homeownership a reality for many who might otherwise struggle to meet the stringent requirements of conventional financing.

Frequently Asked Questions

What is considered a first-time homebuyer?

A first-time homebuyer is generally defined as an individual who has not owned a primary residence for at least the past three years. This definition can also include someone who has never owned a home, a single parent who has only owned a home with a former spouse, or an individual who has only owned a property not affixed to a permanent foundation. Specific criteria may vary depending on the loan program or assistance initiative, so it is important to check the exact definitions for any programs you are considering.

How much money do I need for a down payment?

The amount needed for a down payment varies significantly based on the type of mortgage and your financial situation. While a 20% down payment is often cited to avoid private mortgage insurance (PMI) on conventional loans, many programs allow for much less. FHA loans, for example, require as little as 3.5% down, while VA and USDA loans can offer 0% down payment options for eligible borrowers. It is crucial to consider not only the down payment but also closing costs, which typically range from 2% to 5% of the home’s purchase price.

What is a mortgage pre-approval?

A mortgage pre-approval is a conditional commitment from a lender to loan you a specific amount of money to purchase a home. This commitment is based on a thorough review of your financial information, including your income, assets, debts, and credit history. A pre-approval letter indicates to sellers that you are a serious and qualified buyer, strengthening your offer in a competitive market. It is more robust than a pre-qualification, which is merely an estimate based on self-reported financial data.

What are closing costs?

Closing costs are a collection of fees and expenses paid at the close of a real estate transaction, beyond the purchase price of the home. These costs can include loan origination fees, appraisal fees, title insurance, attorney fees, recording fees, and prepaid expenses like property taxes and homeowner’s insurance. Typically, closing costs range from 2% to 5% of the home’s purchase price and are paid by the buyer, seller, or split between them, depending on the negotiation and local customs.

Should I get a home inspection?

Yes, a home inspection is highly recommended for first-time homebuyers. A professional home inspection provides an objective evaluation of the property’s condition, identifying potential issues with the structure, systems (HVAC, plumbing, electrical), and appliances. This allows buyers to be fully aware of any necessary repairs or maintenance before finalizing the purchase. The inspection report can also serve as a basis for negotiating with the seller for repairs or credits, or even for withdrawing the offer if significant, undisclosed problems are found, protecting your investment and peace of mind.

Embarking on the journey to homeownership is a significant milestone, and being well-informed is the best way to navigate the process with confidence. By understanding your financial standing, exploring all available mortgage and assistance options, and partnering with experienced professionals, you can make a sound investment and achieve your dream of owning a home. The path may have its complexities, but with careful planning and a clear understanding of each step, you can successfully transition from a first-time buyer to a proud homeowner.

Most Viewed