Mortgage refinancing involves replacing an existing home loan with a new one, a financial strategy that can significantly reduce monthly payments, lower interest rates, or provide access to home equity for various purposes. This process is a critical tool for homeowners to optimize their financial situation and adapt to changing market conditions, making understanding the diverse types of refinancing crucial for informed decisions, explains Mabry Management specialists.

Homeowners often seek to lower their monthly payments or shorten their loan term, and a rate-and-term refinance allows them to achieve these goals by adjusting the interest rate or repayment period without altering the principal balance. Understanding Rate-and-Term Refinance

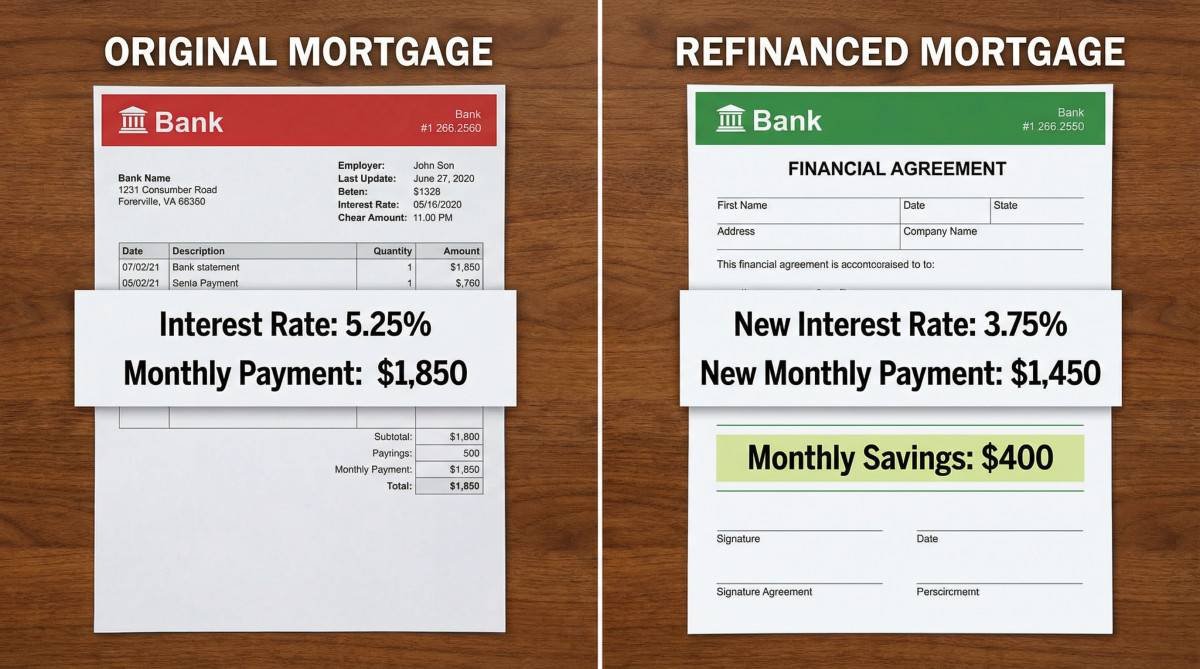

Rate-and-term refinancing is a common option for homeowners seeking to adjust their loan’s interest rate or repayment period without altering the principal balance. This type of refinance is ideal for those looking to reduce their monthly mortgage payments by securing a lower interest rate or to pay off their mortgage faster by switching to a shorter loan term. For example, moving from a 30-year fixed-rate mortgage to a 15-year fixed-rate mortgage can substantially decrease the total interest paid over the life of the loan, albeit with potentially higher monthly payments. Eligibility typically depends on current market rates being lower than the existing mortgage rate and the homeowner’s creditworthiness. [1]

This refinancing option is particularly attractive when prevailing interest rates are lower than the rate on an existing mortgage. By securing a lower rate, homeowners can significantly reduce their monthly mortgage payments, freeing up funds for other financial priorities. Alternatively, homeowners can opt for a shorter loan term, such as converting a 30-year mortgage to a 15-year term. While this often results in higher monthly payments, it can lead to substantial savings on total interest paid over the life of the loan and accelerate equity building. The decision between a lower payment and a shorter term depends on individual financial goals and capacity. [1]

| Feature | Description | Ideal Scenario |

|---|---|---|

| Interest Rate Adjustment | Securing a lower interest rate on the new mortgage. | When current market rates are below your existing mortgage rate. |

| Loan Term Modification | Changing the length of the repayment period (e.g., 30 years to 15 years). | To save on total interest (shorter term) or reduce monthly payments (longer term). |

| No Cash Out | The principal balance remains largely the same, excluding closing costs. | When the primary goal is to adjust rate or term, not to access home equity. |

| Eligibility | Good credit score, stable income, and sufficient home equity. | Homeowners with strong financial standing looking to optimize mortgage terms. |

For homeowners needing to access their home equity for significant expenses like renovations or debt consolidation, a cash-out refinance provides liquid funds by replacing the existing mortgage with a larger loan. Exploring Cash-Out Refinance Opportunities

A cash-out refinance enables homeowners to convert a portion of their home equity into liquid funds by taking out a new mortgage for a larger amount than their current outstanding balance. The difference between the new loan amount and the old balance is disbursed to the homeowner in cash at closing. This option is frequently utilized for significant expenses such as home renovations, debt consolidation, or educational funding. For instance, a homeowner with $200,000 in equity might refinance their $150,000 mortgage into a $250,000 loan, receiving $100,000 in cash. Lenders typically require a substantial amount of equity to qualify, often allowing borrowers to retain at least 20% equity after the refinance. [2]

This type of refinancing is particularly beneficial when the funds are used to improve the property’s value or to pay off high-interest debt, such as credit card balances. By consolidating debt into a mortgage, homeowners can often secure a much lower interest rate, reducing their overall monthly debt obligations. However, it is crucial to recognize that a cash-out refinance increases the total debt secured by the home and may result in higher monthly mortgage payments or an extended repayment period. Homeowners must carefully weigh the benefits of immediate cash against the long-term costs of increased mortgage debt. [2]

| Consideration | Detail | Impact on Homeowner |

|---|---|---|

| Equity Requirement | Must have significant equity, usually retaining 20% post-refinance. | Limits the amount of cash available to borrow. |

| Interest Rates | Often slightly higher than rate-and-term refinance rates. | Increases the cost of borrowing the additional funds. |

| Closing Costs | Applicable to the new, larger loan amount. | Reduces the net cash received from the refinance. |

| Risk Factor | Increases total mortgage debt and potentially monthly payments. | Higher risk of foreclosure if payments become unaffordable. |

Government-backed loan holders (FHA, VA, USDA) can benefit from streamline refinance programs, which offer an expedited process to secure more favorable terms with reduced paperwork and underwriting requirements, making refinancing quicker and less burdensome. The Benefits of Streamline Refinance Programs

Streamline refinance programs offer an expedited process for homeowners with government-backed loans (FHA, VA, USDA) to secure more favorable terms with reduced paperwork and underwriting requirements. These programs are designed to make refinancing quicker and less burdensome, often waiving the need for a new appraisal or extensive credit checks. For example, an FHA Streamline Refinance allows existing FHA loan holders to lower their interest rate or change their loan term with minimal documentation, provided they have a history of on-time payments. The primary goal of a streamline refinance is to provide a clear financial benefit to the borrower, such as a lower interest rate or reduced monthly payment. [3]

These programs are particularly advantageous for borrowers who may not qualify for a traditional refinance due to lower credit scores or insufficient equity. The reduced documentation requirements, such as waiving income verification or property appraisals, can significantly shorten the closing timeline and lower upfront costs. However, it is important to note that streamline refinances typically do not allow for cash-out options; their primary purpose is to improve the terms of the existing loan. Eligibility criteria vary by loan type (FHA, VA, USDA) but generally require a history of on-time mortgage payments. [3]

| Program Type | Key Benefit | Eligibility | Limitations |

|---|---|---|---|

| FHA Streamline | Lower interest rate, reduced monthly payments, less paperwork. | Existing FHA loan, on-time payments, net tangible benefit. | No cash-out, mortgage insurance still required. |

| VA Streamline (IRRRL) | Lower interest rate, reduced monthly payments, no appraisal. | Existing VA loan, on-time payments, net tangible benefit. | No cash-out, occupancy requirement. |

| USDA Streamline | Lower interest rate, no appraisal or credit check for some. | Existing USDA loan, on-time payments, net tangible benefit. | Limited to rural properties, no cash-out. |

Homeowners with available lump sums can reduce their principal or those without upfront cash can avoid closing costs through cash-in or no-closing cost refinances, respectively, each offering distinct financial advantages and considerations for long-term savings. Considering Cash-In and No-Closing Cost Refinance

Cash-in refinancing involves making a lump-sum payment at closing to reduce the principal balance of the new mortgage, which can help homeowners achieve a lower loan-to-value (LTV) ratio, qualify for better interest rates, or eliminate private mortgage insurance (PMI). Conversely, a no-closing cost refinance allows homeowners to avoid upfront closing costs by rolling these fees into the new loan or accepting a slightly higher interest rate. While appealing for those without immediate cash, this option can result in higher overall costs over the loan’s lifetime. A careful calculation of the break-even point is essential to determine if the long-term savings outweigh the increased interest. [4]

Cash-in refinances are particularly useful for homeowners who have received a financial windfall, such as an inheritance or bonus, and wish to apply it directly to their mortgage. By reducing the principal balance, they can often secure a lower interest rate, decrease their monthly payments, or even remove PMI, which can lead to significant long-term savings. This strategy is also beneficial for those who are ‘underwater’ on their mortgage, meaning they owe more than their home is worth, as it can help them regain equity. [4]

No-closing cost refinances, while attractive for their lack of upfront expenses, typically involve either a higher interest rate or the addition of closing costs to the loan principal. This means that while no cash is required at closing, the homeowner will pay more over the life of the loan through increased interest or a larger loan amount. This option is best suited for homeowners who plan to sell their home within a few years, as they may not stay in the home long enough for the higher interest costs to negate the savings from avoiding upfront closing costs. [4]

| Refinance Type | Key Feature | Primary Benefit | Potential Drawback |

|---|---|---|---|

| Cash-In Refinance | Lump-sum payment reduces principal. | Lower LTV, better rates, PMI removal. | Requires significant upfront cash. |

| No-Closing Cost Refinance | No upfront closing costs. | Avoids immediate out-of-pocket expenses. | Higher interest rate or larger loan amount, increasing total cost over time. |

FAQ Section

What is mortgage refinancing?

Mortgage refinancing involves replacing your current home loan with a new one, often to obtain a lower interest rate, change the loan term, or access home equity. It is a new loan that pays off the old one.

When is the best time to refinance?

The optimal time to refinance is typically when interest rates are significantly lower than your current mortgage rate, or when your credit score has improved, allowing you to qualify for better loan terms. It’s also beneficial if you need to access home equity for large expenses.

How does a cash-out refinance work?

A cash-out refinance allows you to borrow against your home’s equity. You take out a new mortgage for more than you currently owe, and the difference is given to you in cash at closing. This cash can be used for various purposes, such as home improvements or debt consolidation.

What are the benefits of a streamline refinance?

Streamline refinances, available for government-backed loans like FHA or VA, offer a quicker and simpler refinancing process with less paperwork, often without requiring an appraisal or extensive credit checks. They are designed to help borrowers secure better loan terms efficiently.

Are there any risks to refinancing?

Yes, risks include incurring new closing costs, potentially extending the loan term, and increasing the total interest paid over time if not carefully planned. A cash-out refinance also increases your debt, which can be risky if not managed responsibly.

Conclusion

Choosing the appropriate mortgage refinancing option requires a thorough evaluation of personal financial goals, current market conditions, and the specific features of each loan type. Whether the objective is to reduce monthly payments, shorten the loan term, or leverage home equity, various refinancing products offer distinct advantages. Homeowners should carefully consider their financial situation, compare interest rates, and assess closing costs to ensure the chosen refinance strategy aligns with their long-term financial well-being. Consulting with a qualified mortgage professional can provide tailored guidance and help navigate the complexities of the refinancing process effectively.

References

[1] Bankrate, “Types of Mortgage Refinance Options,” https://www.bankrate.com/mortgages/choose-the-right-kind-of-refinance/

[2] Rocket Mortgage, “Types of mortgage refinance: Which option is right for you?”, https://www.rocketmortgage.com/learn/types-of-refinance

[3] Fannie Mae, “Mortgage refinancing options,” https://yourhome.fanniemae.com/own/refinance-options

[4] Freedom Mortgage, “A Guide to Home Refinance Loan Types,” https://www.freedommortgage.com/learn/refinancing/types-of-mortgage-refinance-loans

Most Viewed