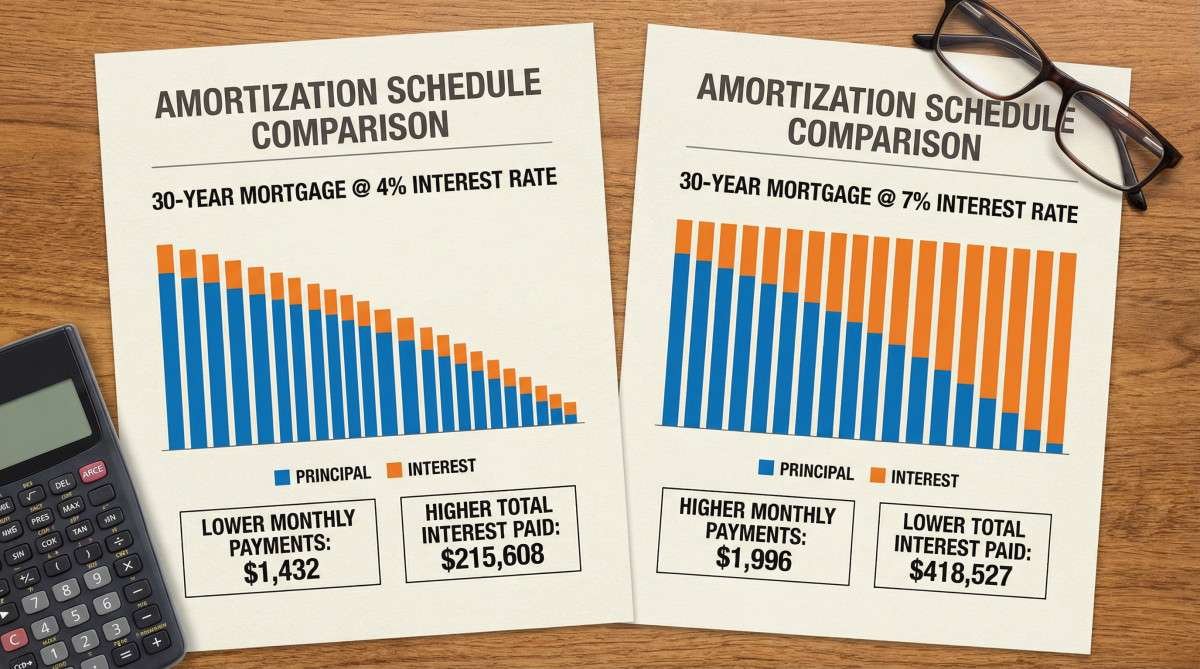

Mortgage interest rates directly influence the total cost of borrowing and the size of your monthly mortgage payments, with even small fluctuations significantly altering the financial burden over the loan’s lifetime, The Maryland and Delaware Group PM experts explain. A higher interest rate means a larger portion of each payment goes towards interest, reducing the principal balance more slowly and increasing the overall amount repaid.

Understanding Mortgage Interest Rates

Mortgage interest rates are the cost of borrowing money to purchase a home, expressed as a percentage of the loan amount, and they are influenced by various economic factors, including inflation, the Federal Reserve’s monetary policy, and the overall health of the housing market. These rates determine how much extra you pay back to the lender beyond the principal, directly impacting your monthly mortgage payment and the total cost of your home over the loan’s term.

Fixed vs. Adjustable Rates

Fixed-rate mortgages maintain the same interest rate for the entire loan term, providing predictable monthly payments, while adjustable-rate mortgages (ARMs) have an initial fixed period followed by periodic adjustments based on market indices, leading to fluctuating payments. The choice between these two types depends on your financial stability, risk tolerance, and expectations for future interest rate movements.

Calculating Monthly Payments

Your monthly mortgage payment is primarily determined by the loan’s principal amount, the interest rate, and the loan term, with a higher interest rate or a shorter loan term generally resulting in larger monthly payments. Lenders use amortization schedules to break down each payment into principal and interest components, showing how the balance decreases over time. Understanding this calculation helps homeowners budget effectively and anticipate their financial commitments.

Principal and Interest

The principal is the original amount of money borrowed, and interest is the cost of borrowing that money, with each monthly payment typically comprising both components. In the early years of a mortgage, a larger portion of the payment goes towards interest, while later payments allocate more towards reducing the principal balance.

Factors Influencing Interest Rates

Several key factors influence mortgage interest rates, including economic indicators like inflation and employment rates, the Federal Reserve’s decisions on the federal funds rate, and the bond market’s performance, all of which contribute to the overall cost of lending. Lenders also consider individual borrower characteristics such as credit score, debt-to-income ratio, and down payment size, as these factors indicate the borrower’s risk profile. Understanding these influences can help prospective homeowners anticipate rate changes and secure more favorable loan terms.

Economic Indicators

Economic indicators such as inflation, unemployment rates, and GDP growth significantly impact mortgage interest rates, as a strong economy often leads to higher rates due to increased demand for credit and concerns about inflation. Conversely, a weaker economy might see lower rates as central banks try to stimulate borrowing and spending. These indicators are closely monitored by lenders and financial markets to forecast future rate movements.

Credit Score and Debt-to-Income

Your credit score and debt-to-income (DTI) ratio are critical personal financial factors that lenders evaluate when determining your mortgage interest rate, with a higher credit score and a lower DTI ratio typically qualifying you for more favorable rates. A strong credit history demonstrates responsible financial management, while a low DTI indicates you can comfortably manage additional debt, both reducing the perceived risk for lenders. Improving these metrics before applying for a mortgage can lead to significant long-term savings.

Impact of Interest Rate Changes

Changes in mortgage interest rates can significantly impact both prospective homebuyers and existing homeowners, influencing affordability, purchasing power, and the overall cost of homeownership. Even a small percentage point shift can alter monthly payments by hundreds of dollars, affecting budget planning and the decision to buy or refinance. Understanding this impact is crucial for making informed financial decisions in the real estate market.

Affordability and Purchasing Power

Mortgage interest rates directly affect a homebuyer’s affordability and purchasing power, as lower rates reduce the monthly payment for a given loan amount, allowing buyers to afford more expensive homes or save on their monthly budget. Conversely, higher rates increase the monthly cost, potentially limiting the price range of homes they can realistically consider. This relationship highlights the importance of securing a favorable interest rate to maximize homeownership opportunities.

Refinancing Opportunities

Refinancing a mortgage involves replacing an existing loan with a new one, often to secure a lower interest rate, reduce monthly payments, or change the loan term, and it becomes particularly attractive when market interest rates drop significantly below your current rate. This strategy can lead to substantial long-term savings and improved financial flexibility, but it’s essential to consider closing costs and the break-even point before committing to a refinance. Evaluating refinancing opportunities can be a smart move for homeowners looking to optimize their mortgage terms.

FAQ: How Does Mortgage Interest Affect Monthly Payments?

Q1: What is the primary way mortgage interest impacts my monthly payment?

Mortgage interest directly increases the total amount you owe each month, as it is the cost charged by the lender for borrowing the principal amount, meaning a higher interest rate results in a larger portion of your monthly payment going towards interest rather than reducing the loan’s principal. This directly translates to a higher overall monthly payment.

Q2: How do changes in interest rates affect my monthly payment on a fixed-rate mortgage?

Changes in market interest rates do not affect your monthly payment on a fixed-rate mortgage once your loan is closed, as the interest rate is locked in for the entire term of the loan, providing stability and predictability in your payments regardless of market fluctuations. Your payment amount remains constant, making budgeting straightforward.

Q3: What is an amortization schedule and how does it relate to interest?

An amortization schedule is a table detailing each periodic loan payment, showing how much of the payment is applied to the principal and how much to interest, with early payments heavily weighted towards interest and later payments more towards principal. This schedule illustrates the gradual reduction of your loan balance over time, clearly demonstrating the impact of interest on your repayment structure.

Q4: Can I reduce the total interest paid over the life of my mortgage?

Yes, you can reduce the total interest paid over the life of your mortgage by making extra principal payments, refinancing to a lower interest rate, or choosing a shorter loan term, all of which accelerate the repayment of the principal balance. Even small additional payments can significantly decrease the overall interest burden and shorten the loan’s duration.

Q5: How does my credit score influence the mortgage interest rate I receive?

Your credit score significantly influences the mortgage interest rate you receive because lenders use it to assess your creditworthiness and the risk of lending to you, with higher credit scores typically qualifying borrowers for lower interest rates. A strong credit history indicates a reliable borrower, leading to more favorable loan terms and substantial savings over the life of the mortgage.

Conclusion

Understanding the intricate relationship between mortgage interest rates and monthly payments is fundamental for anyone navigating the real estate market. The interest rate directly dictates the financial commitment of homeownership, influencing both immediate budgetary concerns and long-term financial health. Factors ranging from global economic indicators to individual credit profiles collectively shape these rates, underscoring the importance of informed decision-making. By grasping how these elements interact, homeowners and prospective buyers can strategically manage their mortgages, optimize their financial outlay, and secure a more stable financial future. This knowledge empowers individuals to make prudent choices, whether securing a new loan or considering refinancing options, ultimately leading to more effective financial planning in the housing sector.

Most Viewed