The deposit required to purchase a house typically ranges from 3% to 20% of the home’s total value, influenced by factors such as the loan program, lender requirements, and the buyer’s financial profile, notes the TrueNest Property Management team. This initial payment is a crucial component of securing a mortgage and demonstrating financial commitment to the property.

Understanding Minimum Deposit Requirements

In many regions, the minimum deposit for a house can be as low as 3% for conventional loans, while government-backed options like VA and USDA loans may require no down payment at all. This varies significantly based on local market conditions, specific lender policies, and the type of mortgage product chosen by the homebuyer.

While a 20% down payment has historically been considered standard, many mortgage programs today allow for much lower initial investments. The specific percentage required often depends on the loan type, the borrower’s creditworthiness, and the property’s value. For instance, first-time homebuyers often qualify for programs with reduced down payment thresholds.

Conventional Loans: Starting at 3%

Conventional loans, which are not insured or guaranteed by the government, can require as little as a 3% down payment for eligible borrowers, particularly first-time homebuyers or those with moderate incomes. However, putting down less than 20% typically necessitates private mortgage insurance (PMI), an additional monthly cost that protects the lender in case of default. PMI can often be removed once sufficient equity is built in the home.

FHA Loans: 3.5% Minimum

Federal Housing Administration (FHA) loans are popular among buyers with lower credit scores or limited savings, requiring a minimum down payment of 3.5% for those with a credit score of 580 or higher. If the credit score is between 500 and 579, a 10% down payment is generally required. FHA loans also involve mortgage insurance premiums (MIPs), both an upfront fee and an annual premium, which can sometimes be removed after a certain period depending on the initial down payment amount and loan term.

VA and USDA Loans: Zero Down Payment Options

For eligible veterans, active-duty service members, and their surviving spouses, VA loans offer the significant advantage of requiring no down payment. Similarly, USDA loans provide zero-down payment options for properties in designated rural areas, aimed at promoting homeownership in less densely populated regions. Both VA and USDA loans have specific eligibility criteria and may include funding fees or guarantee fees, respectively, which are typically financed into the loan.

Factors Influencing Your Deposit Amount

The ideal deposit amount for a house is influenced by individual financial circumstances, including credit score, debt-to-income ratio, and available savings, as well as the specific property price and the prevailing mortgage interest rates in the local housing market. A higher deposit can lead to more favorable loan terms and lower monthly payments.

Beyond the minimum requirements, several factors play a crucial role in determining how much you should realistically put down on a house. These considerations can impact your mortgage terms, monthly payments, and overall financial health.

Credit Score and Loan Eligibility

Your credit score is a significant determinant of loan eligibility and the interest rate you receive. A higher credit score generally opens doors to more favorable loan products, potentially allowing for a lower down payment while still securing competitive interest rates. Conversely, a lower credit score might necessitate a larger down payment to mitigate the lender’s risk.

Property Price and Loan-to-Value (LTV) Ratio

The purchase price of the home directly influences the absolute dollar amount of your down payment, even if the percentage remains constant. Lenders use the loan-to-value (LTV) ratio, which compares the loan amount to the home’s appraised value, to assess risk. A lower LTV (meaning a higher down payment) often results in better loan terms and can help avoid PMI.

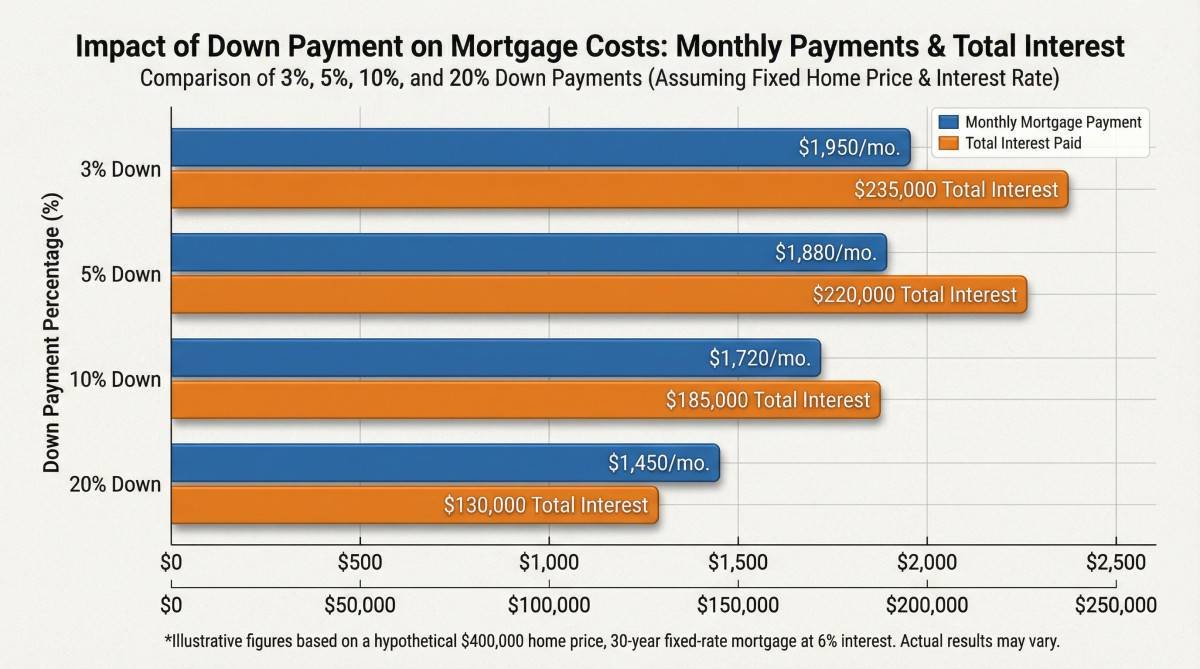

Impact on Monthly Payments and Interest Rates

A larger down payment reduces the principal loan amount, which in turn lowers your monthly mortgage payments. Furthermore, lenders often offer lower interest rates to borrowers who make substantial down payments, as it signifies a reduced risk. Over the life of a 30-year mortgage, even a slightly lower interest rate can result in significant savings.

Closing Costs and Other Upfront Expenses

It’s important to remember that the down payment is not the only upfront cost associated with buying a home. Closing costs, which typically range from 2% to 5% of the loan amount, include various fees such as appraisal fees, title insurance, and legal fees. These costs must be paid at closing and should be factored into your overall savings plan, separate from your down payment.

Benefits of Larger and Smaller Down Payments

Deciding on the size of your down payment involves weighing the advantages of a lower monthly mortgage payment and reduced interest costs against the benefit of retaining more liquid assets for other investments or immediate home expenses. The optimal choice aligns with individual financial goals and risk tolerance.

Advantages of a Larger Down Payment

- Lower Monthly Payments: A larger initial investment directly reduces the loan principal, resulting in lower monthly mortgage payments. This can significantly ease the financial burden of homeownership.

- Reduced Interest Paid Over Time: With a smaller loan amount, you pay less interest over the life of the mortgage, leading to substantial long-term savings.

- Avoid Private Mortgage Insurance (PMI): If you put down 20% or more on a conventional loan, you can typically avoid paying PMI, which is an extra monthly expense.

- More Favorable Loan Terms: Lenders often view borrowers with larger down payments as lower risk, potentially offering better interest rates and more flexible loan terms.

- Increased Equity from Day One: A larger down payment means you own a greater portion of your home from the start, building equity faster.

- Stronger Offer in Competitive Markets: In a seller’s market, a substantial down payment can make your offer more attractive to sellers, signaling financial stability and a higher likelihood of closing.

Advantages of a Smaller Down Payment

- Faster Entry into Homeownership: A lower down payment can accelerate your timeline for buying a home, especially beneficial in rising markets.

- Preserve Savings for Other Needs: Keeping more cash on hand allows you to cover unexpected home repairs, renovations, or maintain a robust emergency fund.

- Investment Opportunities: Instead of tying up a large sum in a down payment, you might choose to invest the difference in other assets that could yield higher returns.

- Access to More Expensive Homes: A smaller down payment can enable you to purchase a more expensive property than you might otherwise afford, by reducing the immediate cash outlay.

- Leveraging Low-Interest Rates: If mortgage interest rates are particularly low, some buyers prefer to finance more of the home’s value and invest their savings elsewhere.

Saving Strategies and Assistance Programs

Prospective homebuyers can employ various saving strategies, such as disciplined budgeting, automating savings transfers, and exploring government-backed or local assistance programs designed to reduce the financial burden of a down payment. These programs often provide grants or low-interest loans to help bridge the gap for eligible buyers.

Accumulating a sufficient down payment can be a significant hurdle for many aspiring homeowners. Fortunately, a combination of personal financial discipline and available assistance programs can make this goal more attainable.

Effective Saving Techniques

- Budgeting and Expense Tracking: Create a detailed budget to identify areas where you can cut back on discretionary spending. Tracking every expense helps in understanding where your money goes and where savings can be maximized.

- Automated Savings: Set up automatic transfers from your checking account to a dedicated savings account each payday. This

ensures consistent saving without conscious effort. - Side Gigs and Extra Income: Consider taking on a part-time job or freelance work to boost your income and direct all additional earnings towards your down payment fund.

- Sell Unused Items: Decluttering your home and selling items you no longer need can provide a quick influx of cash for your savings.

- Delay Major Purchases: Postpone significant expenses like a new car or expensive vacations to prioritize saving for your home.

Down Payment Assistance Programs

Many government agencies and non-profit organizations offer programs to help individuals and families achieve homeownership. These programs vary by location and eligibility criteria but can significantly reduce the upfront financial burden.

- First-Time Homebuyer Programs: These programs often provide grants, low-interest loans, or deferred-payment loans specifically for individuals purchasing their first home. Eligibility typically depends on income limits, credit scores, and the property location.

- State and Local Programs: Many states, counties, and cities offer their own down payment assistance programs. These can be particularly beneficial as they are tailored to local housing markets and needs.

- Employer-Assisted Housing Programs: Some employers offer assistance to their employees for home purchases, which can include grants or forgivable loans.

- Community Development Financial Institutions (CDFIs): These organizations provide financial services to underserved communities and may offer flexible mortgage products and down payment assistance.

Frequently Asked Questions

What is the average down payment for a house?

The average down payment for a house varies significantly by region and buyer type. For all buyers, it can range from 10% to 20%, while first-time homebuyers often put down less, sometimes as low as 3% to 5%.

Can I buy a house with no down payment?

Yes, certain loan programs, such as VA loans for eligible military personnel and USDA loans for properties in designated rural areas, offer zero-down payment options. These programs have specific eligibility criteria that must be met.

Does a larger down payment always mean a lower interest rate?

Generally, a larger down payment reduces the lender’s risk, which often translates to a lower interest rate on your mortgage. However, other factors like your credit score and overall financial health also play a significant role in determining your interest rate.

What are closing costs, and are they part of the down payment?

Closing costs are fees paid at the close of a real estate transaction, typically ranging from 2% to 5% of the loan amount. They are separate from the down payment and cover various expenses like appraisal fees, title insurance, and legal fees.

How can I find down payment assistance programs?

You can find down payment assistance programs through local housing authorities, state housing finance agencies, non-profit organizations, and some lenders. Many programs are designed for first-time homebuyers or those with specific income qualifications.

Conclusion

Determining the appropriate down payment for a house is a multifaceted decision influenced by individual financial capacity, loan program specifics, and personal homeownership goals. Minimum requirements can be as low as 0% for certain government-backed loans, or 3% for conventional mortgages. A larger down payment often yields benefits such as lower interest rates, reduced monthly payments, and the avoidance of private mortgage insurance. Conversely, a smaller down payment can facilitate quicker entry into the housing market and preserve liquid assets for other investments or immediate home-related expenses. Prospective buyers should carefully assess their financial situation, explore available assistance programs, and consider both the short-term and long-term implications of their down payment choice to make an informed decision that aligns with their financial well-being.

Most Viewed