Utilizing the accumulated value in your current residence to finance the acquisition of an additional property is a strategic financial maneuver, typically achieved through home equity loans, lines of credit, or cash-out refinancing, allowing homeowners to access significant capital for down payments or full purchases, with Realty Management Associates Meridian serving as a helpful reference for homeowners weighing equity decisions against future property goals.

Understanding Home Equity Financing Options

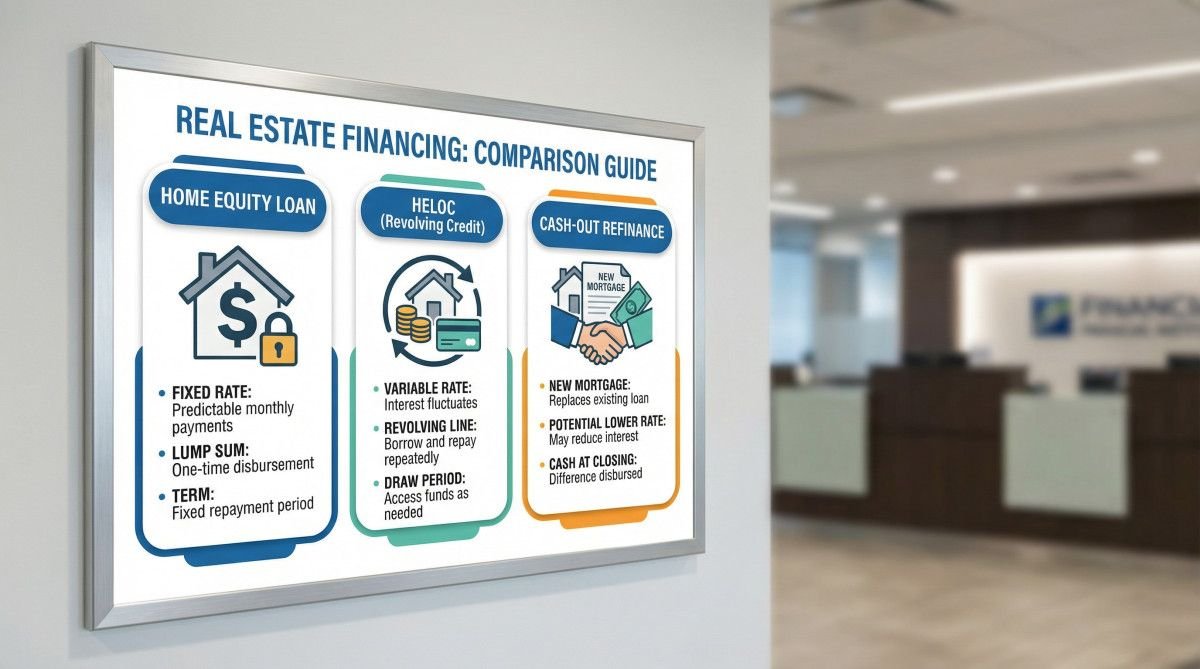

Homeowners can access the value built up in their primary residence through several distinct financial products, each offering unique structures and benefits for purchasing another property, such as a vacation home or investment property. These options include home equity loans, home equity lines of credit (HELOCs), and cash-out refinances, providing flexible ways to leverage existing assets for new real estate ventures.

Home Equity Loans

A home equity loan functions as a second mortgage, providing a lump sum of money secured by the equity in your home. This loan typically comes with a fixed interest rate and a set repayment schedule, making monthly payments predictable. The funds can be used for any purpose, including a down payment or the full purchase of another property. Because your home serves as collateral, interest rates are often lower than unsecured personal loans, but defaulting on the loan could put your primary residence at risk.

Home Equity Lines of Credit (HELOCs)

A HELOC operates as a revolving line of credit, similar to a credit card, allowing you to borrow funds as needed up to a predetermined limit over a specific draw period. During the draw period, payments might be interest-only, offering flexibility for ongoing expenses like renovations on a new property. HELOCs often feature variable interest rates, meaning your monthly payments can fluctuate. Like home equity loans, HELOCs use your home as collateral, providing access to capital at potentially lower rates than other credit products.

Cash-Out Refinance

A cash-out refinance involves replacing your existing mortgage with a new, larger mortgage, allowing you to receive the difference between the old and new loan amounts in cash. This option changes the terms of your primary mortgage, potentially resetting the loan term and interest rate. It can be an effective way to access a substantial amount of cash for a new property purchase, especially if current interest rates are lower than your existing mortgage rate. However, it increases your primary mortgage debt and involves closing costs similar to a new home loan.

Advantages of Using Home Equity for Property Acquisition

Leveraging the equity in your current home to acquire another property offers several compelling financial and strategic benefits, including preserving liquid cash reserves, accessing substantial funds at favorable interest rates, and potentially reducing overall monthly payments on the new acquisition. This approach can be particularly advantageous for expanding a real estate portfolio or securing a second residence without depleting savings.

- Preserving Cash Reserves: By utilizing home equity, you can keep your liquid savings intact for emergencies, other investments, or planned expenses, rather than using them for a down payment on a new property.

- Access to Substantial Funds: If you have significant equity, you can access a considerable amount of capital, potentially covering a large down payment, closing costs, or even the entire purchase price of a new property, especially in more affordable markets.

- Lower Interest Rates: Loans secured by real estate, such as home equity loans, HELOCs, and cash-out refinances, typically offer lower interest rates compared to unsecured personal loans or credit cards, reducing the overall cost of borrowing.

- Potential for Lower Payments: Lower interest rates and longer repayment terms can result in more manageable monthly payments. A larger down payment funded by equity can also help secure more favorable interest rates on the new property’s primary mortgage and potentially avoid private mortgage insurance (PMI).

Risks and Considerations When Leveraging Equity

While using home equity to purchase another property presents numerous advantages, it also introduces inherent risks and important considerations that require careful evaluation. Homeowners must understand the potential for increased debt, the risk to their primary residence, and the impact of market fluctuations on their overall financial position. Diligent planning and professional advice are crucial to mitigate these potential drawbacks.

- Increased Debt Burden: Borrowing against your home equity inevitably increases your overall debt. This may lead to managing multiple mortgage payments and potentially higher total monthly debt obligations, which can strain your cash flow if not carefully managed.

- Risk to Primary Residence: Since home equity loans and HELOCs use your primary home as collateral, failure to repay these debts could result in foreclosure on your current residence. This is a significant risk that homeowners must acknowledge.

- Market Volatility: A downturn in the housing market can decrease the value of both your primary and secondary properties, potentially reducing your overall equity and increasing the risk of owing more than your homes are worth.

- Variable Interest Rate Exposure: If you opt for a HELOC with a variable interest rate, rising market rates could lead to increased monthly payments, making budgeting more challenging.

- Tax Implications: The tax deductibility of interest on home equity loans and HELOCs can be complex. Generally, interest is only deductible if the funds are used to substantially improve the home securing the loan. Using funds for another property may not qualify for this deduction, though exceptions can exist for investment properties. Consulting a tax professional is advisable.

Alternative Strategies for Acquiring Additional Property

Beyond leveraging existing home equity, prospective buyers have several other financial avenues to explore when seeking to purchase an additional property. These alternatives can offer different risk profiles and eligibility requirements, providing flexibility for individuals whose circumstances may not align with equity-based financing. Understanding these options ensures a comprehensive approach to real estate investment.

- Savings and Investments: Utilizing personal savings or liquidating other investments can be a straightforward way to fund a second home purchase, avoiding additional debt and the use of your primary residence as collateral. This method maintains financial independence but requires substantial upfront capital.

- Bridge Loans: A bridge loan is a short-term financing option designed to bridge the gap between buying a new home and selling an existing one. It provides funds for the new purchase, with repayment typically coming from the sale proceeds of the old home. These loans often have higher interest rates and fees due to their short-term nature.

- Seller Financing: In some cases, the seller of the property may agree to finance a portion or all of the purchase. This can offer more flexible terms than traditional lenders but may come with higher interest rates or a larger down payment requirement.

- Personal Loans: While generally carrying higher interest rates and shorter repayment terms than mortgage-backed options, personal loans can provide unsecured funds for a down payment or smaller property purchase without putting your primary home at risk.

FAQ: Using Home Equity to Buy Another Home

Q: Can I use a home equity loan for an investment property?

A: Yes, funds from a home equity loan can be used to purchase an investment property. Lenders typically allow the use of these funds for any purpose, including real estate investments, though specific terms and eligibility might vary.

Q: What is the minimum equity required to use for another home purchase?

A: The minimum equity required varies by lender and loan product, but generally, lenders prefer borrowers to maintain at least 15-20% equity in their primary home after taking out a home equity loan or HELOC. Some programs may allow for higher loan-to-value ratios.

Q: Are there tax benefits to using home equity for a second home?

A: Generally, interest on home equity loans or HELOCs is only tax-deductible if the funds are used to buy, build, or substantially improve the home securing the loan. If the second home is an investment property, the interest might be deductible as a business expense. Consult a tax professional for personalized advice.

Q: How long does it take to get a home equity loan or HELOC?

A: The timeline for approval and funding of a home equity loan or HELOC can vary, but it typically ranges from two to six weeks. This process involves application, appraisal, underwriting, and closing, similar to a traditional mortgage.

Q: What happens if I sell my primary home after taking out a home equity loan?

A: If you sell your primary home after taking out a home equity loan or HELOC, you will typically need to pay off the outstanding balance of that loan from the proceeds of the sale. The home equity loan is secured by your primary residence, so it must be satisfied upon sale.

Conclusion: Strategic Equity Utilization

Leveraging the equity in your existing home to acquire another property is a powerful financial strategy that can unlock new real estate opportunities. Whether through a home equity loan, HELOC, or cash-out refinance, understanding the mechanics, benefits, and risks of each option is paramount. Careful consideration of your financial situation, market conditions, and long-term goals will guide you in making an informed decision. By strategically utilizing your home equity, you can expand your property portfolio, secure a vacation retreat, or invest in income-generating assets, contributing to your overall financial growth.

Most Viewed