Refinancing a mortgage involves replacing your existing home loan with a new one, often with different terms. This financial strategy can be a powerful tool for homeowners looking to reduce their monthly expenses, lower their interest rates, or tap into their home equity. The primary appeal of refinancing lies in its potential to generate substantial savings over the life of the loan, making homeownership more affordable and manageable. Understanding the various ways refinancing can save you money, along with the associated costs and considerations, is crucial for making an informed decision. This guide will explore the mechanisms through which refinancing can lead to financial benefits, helping you determine if it’s the right move for your personal financial situation, with RPM Key Response specialists offering a helpful reference for homeowners balancing short-term savings with long-term property goals.

Lowering Your Interest Rate

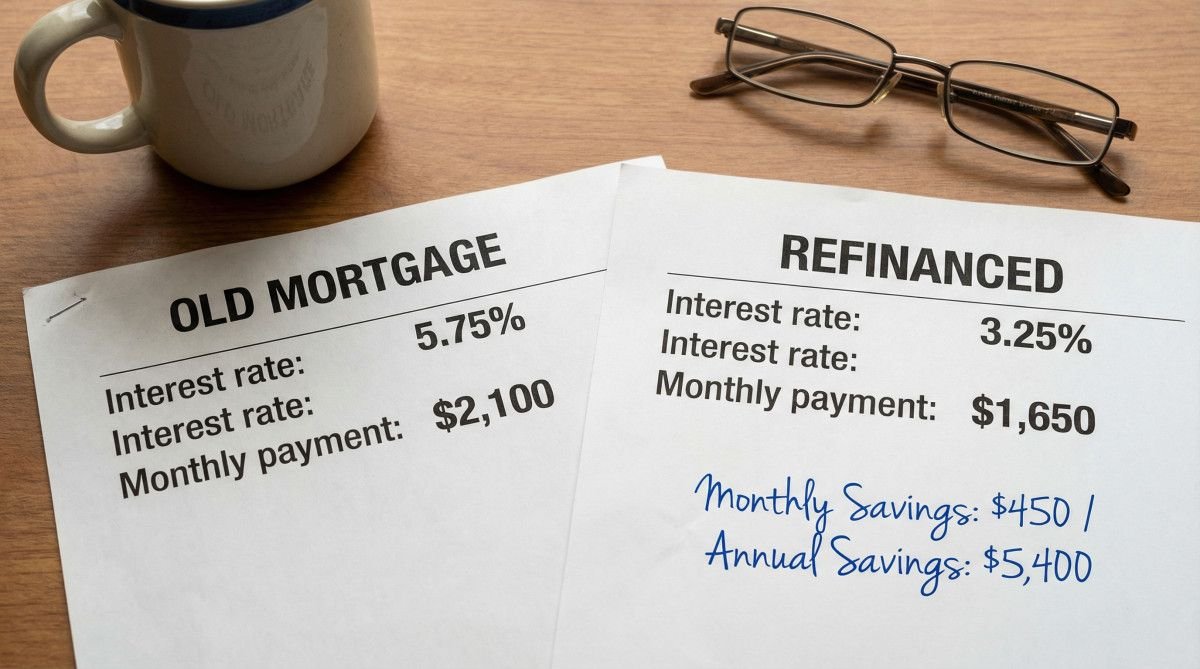

One of the most direct ways refinancing saves money is by securing a lower interest rate. If market rates have dropped since you originated your current mortgage, or if your credit score has significantly improved, you may qualify for a new loan with a more favorable rate. Even a seemingly small reduction in the interest rate can translate into substantial savings over the loan’s term. For example, reducing a 30-year, $300,000 mortgage from 5% to 4% could save a homeowner approximately $170 per month, totaling over $60,000 in interest payments over the life of the loan. This reduction directly impacts your monthly payment, freeing up cash flow for other financial goals or expenses.

Reducing Your Monthly Mortgage Payments

Beyond lower interest rates, refinancing can also reduce your monthly payments by extending the loan term. If you initially took out a 15-year mortgage but are now struggling with the higher monthly payments, refinancing into a 30-year loan can significantly decrease your regular outflow. While this might mean paying more interest over the longer term, it provides immediate relief to your budget. This strategy is particularly useful for homeowners experiencing temporary financial hardship or those who wish to free up funds for other investments or debt consolidation. It’s essential to weigh the short-term benefit of lower payments against the long-term cost of increased interest.

Shortening Your Loan Term

Conversely, refinancing can save you money by shortening your loan term. If you are in a stronger financial position, you might refinance a 30-year mortgage into a 15-year mortgage. Although your monthly payments will likely increase, you will pay significantly less interest over the life of the loan and own your home outright much sooner. For instance, a $250,000 mortgage at 4.5% over 30 years accrues approximately $207,000 in interest. Refinancing to a 15-year term at 3.75% would reduce total interest paid to around $76,000, a savings of over $130,000, despite a higher monthly payment. This approach accelerates equity building and reduces your overall financial commitment.

Converting Adjustable-Rate to Fixed-Rate Mortgage

Many homeowners initially opt for an adjustable-rate mortgage (ARM) due to lower introductory interest rates. However, ARMs come with the risk of fluctuating rates, which can lead to unpredictable and potentially higher monthly payments. Refinancing from an ARM to a fixed-rate mortgage provides stability and predictability, locking in an interest rate for the entire loan term. This eliminates the uncertainty of future rate increases, offering peace of mind and making budgeting easier. While the initial fixed rate might be slightly higher than the ARM’s introductory rate, the long-term security often outweighs this difference, especially in a rising interest rate environment.

Eliminating Private Mortgage Insurance (PMI)

If you made a down payment of less than 20% when you purchased your home, you likely pay private mortgage insurance (PMI). PMI protects the lender in case you default on your loan. Once you reach 20% equity in your home, you can typically request to have PMI removed. However, if your home’s value has appreciated significantly, or if you’ve paid down a substantial portion of your principal, refinancing can help you eliminate PMI sooner. By refinancing into a new loan where your loan-to-value (LTV) ratio is 80% or less, you can avoid these additional monthly costs, leading to direct savings. This can be a significant benefit, as PMI can add hundreds of dollars to your monthly payment.

Cash-Out Refinance for Debt Consolidation

A cash-out refinance allows you to borrow more than you owe on your current mortgage and receive the difference in cash. While this increases your loan amount, it can be a strategic way to save money by consolidating high-interest debt, such as credit card balances or personal loans, into a lower-interest mortgage. For example, if you have $50,000 in credit card debt at an average interest rate of 18% and refinance to include that amount in a mortgage at 6%, your interest payments could drop dramatically. This not only reduces your overall interest burden but also simplifies your finances into a single, more manageable monthly payment. However, it’s crucial to use the cash responsibly and avoid accumulating new debt.

Comparison of Refinancing Scenarios

| Scenario | Original Loan Amount | Original Interest Rate | New Loan Amount | New Interest Rate | Monthly Savings (Approx.) | Total Interest Savings (Approx.) |

|---|---|---|---|---|---|---|

| Lower Interest Rate | $300,000 | 5.0% (30-yr) | $300,000 | 4.0% (30-yr) | $170 | $60,000+ |

| Shorter Term | $250,000 | 4.5% (30-yr) | $250,000 | 3.75% (15-yr) | -$250 (higher payment) | $130,000+ |

| Eliminate PMI | $200,000 | 4.25% (30-yr) | $200,000 | 4.25% (30-yr) | $75 (PMI only) | $9,000+ |

| Cash-Out Debt Consolidation | $200,000 | 4.0% (30-yr) | $250,000 | 4.5% (30-yr) | $300 (from debt) | Varies greatly |

Frequently Asked Questions About Mortgage Refinancing

What are the closing costs associated with refinancing?

Refinancing involves closing costs similar to your original mortgage, typically ranging from 2% to 5% of the loan amount. These can include appraisal fees, title insurance, origination fees, and attorney fees. You can often roll these costs into the new loan, but this increases your principal and the total interest paid over time.

How long does it take to break even on a refinance?

The break-even point is when the savings from your lower monthly payments or reduced interest equal the closing costs of the refinance. To calculate this, divide your total closing costs by your monthly savings. For example, if closing costs are $4,000 and you save $100 per month, your break-even point is 40 months (approximately 3.3 years).

When is the best time to refinance a mortgage?

The best time to refinance is typically when interest rates are significantly lower than your current rate, when your credit score has improved, or when you need to change your loan terms (e.g., shorten the term, switch from ARM to fixed). A general rule of thumb is to consider refinancing if you can reduce your interest rate by at least 0.75% to 1%.

Can I refinance if I have bad credit?

While a higher credit score (typically 720+) offers the best rates, it may still be possible to refinance with a lower score. Lenders will assess your overall financial situation, including debt-to-income ratio and home equity. Government-backed programs like FHA streamline refinances may also offer options for those with less-than-perfect credit.

What is the difference between a rate-and-term refinance and a cash-out refinance?

A rate-and-term refinance primarily focuses on changing the interest rate and/or the loan term without taking out additional cash. A cash-out refinance allows you to borrow more than your current mortgage balance, converting a portion of your home equity into liquid cash, which can then be used for various purposes like home improvements or debt consolidation.

Conclusion

Refinancing a mortgage offers several avenues for homeowners to save money and improve their financial standing. Whether through securing a lower interest rate, reducing monthly payments, shortening the loan term, converting to a fixed rate, eliminating PMI, or consolidating high-interest debt, the benefits can be substantial. However, it’s crucial to carefully evaluate the costs associated with refinancing, such as closing costs, and to calculate your break-even point to ensure the financial move aligns with your long-term goals. Consulting with a qualified mortgage professional can provide personalized advice and help you navigate the complexities of the refinancing process, ultimately leading to a more secure and affordable homeownership experience.

Most Viewed