Buying a home is often the largest financial transaction an individual undertakes, making the purchase agreement a document of paramount importance. This legally binding contract outlines the terms and conditions between a buyer and seller, detailing everything from the property’s description to the closing date. Understanding its key clauses is not merely advisable; it is essential for protecting your interests and ensuring a smooth transaction. A poorly understood or overlooked clause can lead to significant financial repercussions or even the collapse of a deal. This article will delve into the critical components of a real estate purchase agreement, highlighting what to look for to safeguard your investment and peace of mind.

Understanding Contingency Clauses

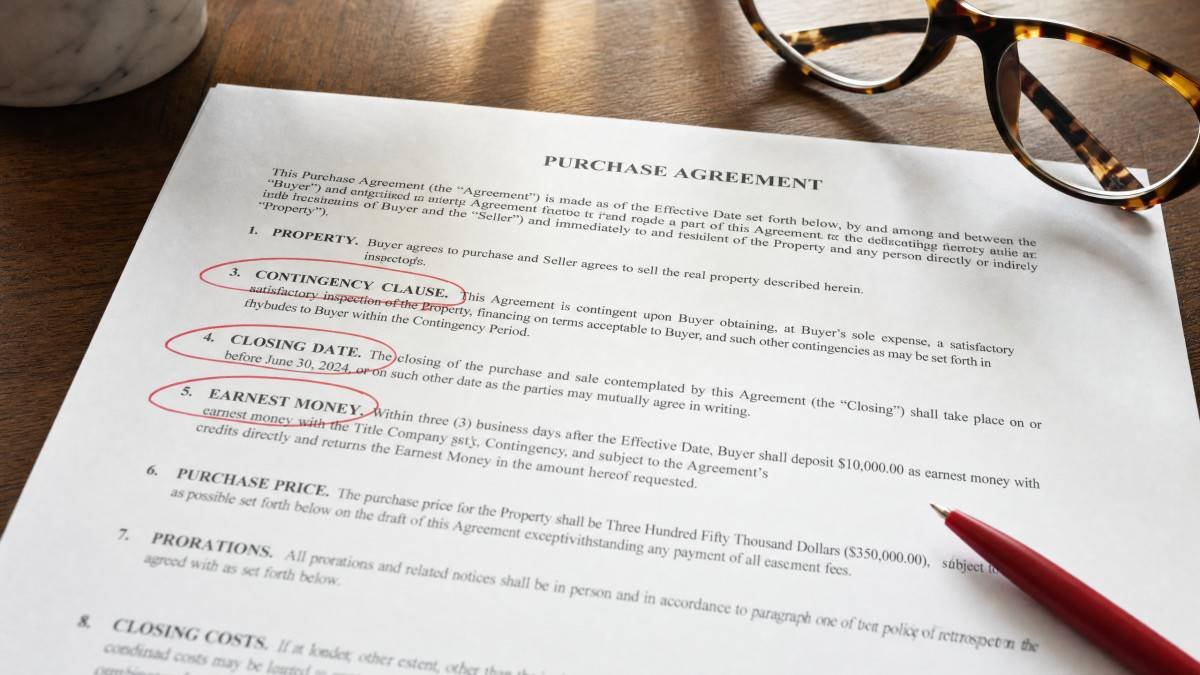

Contingency clauses are conditions that must be met for the purchase agreement to become fully binding, offering crucial protection to buyers by allowing them to withdraw from the deal without penalty if certain events do not occur. These clauses act as safety nets, addressing potential issues such as financing approval, property inspections, and appraisal outcomes. Without them, a buyer could be legally obligated to purchase a property even if unforeseen problems arise, leading to considerable financial strain or legal disputes. For instance, a common financing contingency might stipulate that the buyer must secure a mortgage within 30 days, or the contract can be voided.

One of the most common and vital is the financing contingency, which typically grants the buyer a specific period, often 15 to 45 days, to secure a mortgage loan. If the buyer is unable to obtain financing within this timeframe, they can usually terminate the contract and reclaim their earnest money deposit. This protects buyers from being locked into a purchase they cannot afford. For example, if a buyer applies for a conventional loan requiring a 20% down payment on a $400,000 home, but their lender denies the application due to a change in their credit score, the financing contingency allows them to walk away. Without it, that $8,000 earnest money deposit could be at risk. This can be a source of mild frustration for sellers, who might prefer a buyer with pre-approved financing, but it’s a non-negotiable safeguard for many buyers.

Another critical safeguard is the home inspection contingency. This clause allows the buyer to have the property professionally inspected for structural defects, system failures, and other material issues within a specified period, commonly 7 to 14 days after contract acceptance. Should the inspection reveal significant problems, the buyer typically has several options: negotiate repairs with the seller, request a credit at closing, or, in severe cases, terminate the agreement. Imagine discovering a faulty HVAC system that requires a $10,000 replacement; an inspection contingency provides the leverage to address this before closing. According to the National Association of Realtors (NAR), home inspections are a leading cause of contract renegotiations, underscoring their importance in identifying potential liabilities.

The appraisal contingency is equally important, especially in fluctuating markets. This clause states that the property must appraise for at least the purchase price. Lenders will not finance a loan for more than the appraised value of the home. If the appraisal comes in lower than the agreed-upon price, the buyer can often renegotiate the price with the seller, pay the difference in cash, or cancel the contract. This protects the buyer from overpaying and ensures the lender isn’t taking on undue risk. For instance, if you agree to pay $350,000 for a home, but the appraisal values it at $330,000, this contingency prevents you from being forced to cover the $20,000 gap out of pocket or from losing your earnest money if you decide not to proceed.

Less common, but still significant, is the home sale contingency. This protects buyers who need to sell their current home before they can afford to purchase a new one. It makes the purchase offer contingent upon the sale of their existing property by a certain date. While this offers immense peace of mind to the buyer, it can make their offer less attractive to sellers, particularly in competitive markets, as it introduces an additional layer of uncertainty and a potentially longer closing timeline. It’s a tough spot to be in when you love a house but know your current home needs to sell first.

Property Description and Inclusions

The property description and inclusions section meticulously defines what is being bought and sold, ensuring both parties have a clear understanding of the physical boundaries and any personal property conveyed with the sale. This clarity prevents future disputes over what constitutes part of the real estate transaction. A precise legal description, rather than just a street address, is crucial for defining the exact parcel of land involved. This section also clarifies whether items like appliances, light fixtures, or window treatments are part of the deal, which can often be a point of contention if not explicitly stated.

The legal description of the property is far more precise than a simple street address. It typically refers to lot and block numbers within a recorded subdivision plat or a metes and bounds description, which uses physical landmarks and directions to define boundaries. This specificity is vital for title companies to accurately transfer ownership and for local governments to assess property taxes. Without a clear legal description, the very subject of the contract could be ambiguous, potentially invalidating the agreement or leading to boundary disputes with neighbors down the line. It’s not uncommon for buyers to skim over this, assuming the address is enough, but it’s a foundational element.

Beyond the land itself, the contract must explicitly detail all fixtures and personal property included in the sale. Fixtures are items permanently attached to the property, such as built-in cabinets, plumbing, and heating systems, which are generally assumed to convey with the sale. However, personal property, like refrigerators, washers, dryers, or even certain decorative light fixtures, must be specifically listed if they are to be included. Ambiguity here can lead to awkward situations on moving day. I once saw a deal almost fall apart because the seller took a custom-built shed that the buyer assumed was a fixture. It was a frustrating misunderstanding that could have been avoided with a simple line in the contract. It’s always best to be overly specific, even for seemingly obvious items like the kitchen stove or the curtains.

Purchase Price and Payment Terms

This section clearly states the agreed-upon purchase price and outlines the financial arrangements for the transaction, including the earnest money deposit, down payment, and the method of financing. It is the financial core of the agreement, dictating how and when funds will change hands. A well-defined payment schedule and clear terms for the earnest money protect both buyer and seller, setting expectations for the financial flow of the transaction. Any discrepancies or vague language here can lead to significant delays or even legal challenges.

The purchase price is, of course, the most prominent figure in this section. It is the total amount the buyer agrees to pay for the property. Alongside this, the contract specifies the earnest money deposit, a sum of money, typically 1% to 5% of the purchase price, that the buyer puts down to show serious intent. This money is held in an escrow account and is usually applied towards the down payment or closing costs. However, it can be forfeited to the seller if the buyer breaches the contract without a valid contingency. For a $300,000 home, an earnest money deposit could be $9,000, a substantial sum that underscores the buyer’s commitment.

Furthermore, the contract details the financing terms. This includes whether the purchase is contingent on the buyer obtaining a new mortgage, assuming an existing mortgage, or paying cash. If a new mortgage is required, the contract will specify the type of loan (e.g., conventional, FHA, VA), the interest rate, and the loan term. These details are crucial because they directly impact the buyer’s monthly payments and overall cost of ownership. For example, a buyer might agree to a 30-year fixed-rate mortgage at 6.5%, and this would be reflected in the agreement. Any deviation from these agreed-upon terms could potentially allow the buyer to back out under a financing contingency.

Closing Date and Possession

The closing date and possession clause establishes the exact timeline for the transfer of ownership and when the buyer can physically move into the property, providing a clear schedule for both parties to prepare for the final stages of the transaction. This section is critical for coordinating logistics, such as moving arrangements, utility transfers, and the final walkthrough. Ambiguity in these dates can lead to significant inconvenience, additional costs, or even legal disputes if one party is not ready to proceed as expected.

The closing date is the day when all legal and financial documents are signed, funds are transferred, and the property title officially passes from seller to buyer. This date is typically set 30 to 60 days after the contract is signed, allowing time for inspections, appraisals, loan processing, and title searches. It’s a firm deadline, and missing it can have consequences. For instance, if the buyer’s lender delays funding, the buyer might be in breach of contract, potentially losing their earnest money or facing penalties. Conversely, if the seller isn’t ready to close, the buyer might be able to demand compensation or terminate the agreement. It’s a date everyone works towards, and any slip-ups can be incredibly stressful.

Equally important is the possession date, which specifies when the buyer gains physical access to the property. Often, this is the same as the closing date, but it can be negotiated to be earlier or later. For example, a seller might request a few days after closing to move out, or a buyer might need to move in a day early. If the seller remains in possession after closing, the contract should outline a per diem rental agreement. This prevents situations where a buyer has closed on a home but cannot move in, leading to unexpected housing costs. Clarity here is paramount; you don’t want to be homeless on closing day because the seller hasn’t moved their belongings out yet.

Disclosures and Representations

Disclosures and representations are statements made by the seller about the property’s condition and history, providing the buyer with crucial information that could influence their decision to purchase or the terms of the agreement. These clauses are designed to protect buyers from hidden defects and ensure transparency in the transaction. Failure to disclose known issues can lead to legal action against the seller, highlighting the importance of honesty and thoroughness in this section. Buyers should review these documents meticulously, as they often reveal significant details about the property.

Seller disclosures are legally mandated documents in most states, requiring sellers to reveal known material defects of the property. These can include issues with the roof, foundation, plumbing, electrical systems, environmental hazards like lead paint or asbestos, and past repairs or insurance claims. For example, a seller might disclose that the basement has a history of minor water intrusion during heavy rains, or that the property is located in a flood zone. While these disclosures don’t necessarily obligate the seller to fix the issues, they provide the buyer with the knowledge to make an informed decision, potentially leading to further inspections or renegotiations. It’s a moment where you realize the house isn’t perfect, and you have to weigh the risks.

Representations and warranties are statements of fact made by the seller about the property at the time of the contract. These might include assurances that the property is not subject to any liens, that all systems are in working order, or that there are no pending legal actions against the property. Unlike disclosures, which focus on known defects, representations are affirmative statements about the property’s current status. If a representation turns out to be false after closing, the buyer may have legal recourse. For instance, if the seller represents that the heating system is fully functional, but it fails a week after closing, the buyer might be able to seek damages. These clauses are vital for establishing a baseline of trust and accountability in the transaction.

Frequently Asked Questions

What is earnest money, and is it refundable?

Earnest money is a deposit showing good faith, typically 1-5% of the purchase price, held in escrow. It is generally refundable if a contingency is not met, but can be forfeited if the buyer breaches the contract without a valid reason.

Can I waive contingencies to make my offer stronger?

Yes, waiving contingencies can make an offer more attractive to sellers, especially in competitive markets, but it significantly increases the buyer’s risk. It means you might be obligated to buy even if financing falls through or major defects are found.

What happens if the seller backs out of the agreement?

If a seller backs out without a valid reason, the buyer may have legal recourse, including suing for specific performance (forcing the sale) or seeking damages for costs incurred. The specific remedies depend on the contract and local laws.

How long does a purchase agreement typically last?

A purchase agreement typically lasts from the date of acceptance until the closing date, which is often 30 to 60 days. The duration is influenced by factors like financing, inspections, and title work.

Should I have an attorney review the purchase agreement?

Yes, it is highly advisable to have a qualified real estate attorney review the purchase agreement before signing. An attorney can identify potential pitfalls, explain complex clauses, and ensure your interests are adequately protected, which is especially important given the significant financial implications.

Conclusion

The real estate purchase agreement is a foundational document in the home-buying journey, laden with clauses that carry significant legal and financial weight. From the protective shield of contingency clauses to the precise definitions of property inclusions and the critical timelines for closing, each section plays a vital role in shaping the transaction. A thorough understanding and careful review of these key provisions are indispensable for any prospective homeowner. While the process can feel overwhelming, taking the time to comprehend these details, perhaps with professional guidance, can prevent costly surprises and ensure that your path to homeownership is as secure and straightforward as possible. Ultimately, knowledge and diligence in reviewing this document are your best allies in making one of life’s most significant investments.

Most Viewed