Embarking on the journey to homeownership is an exciting prospect, often filled with anticipation and a touch of apprehension. One of the most crucial early steps is securing mortgage pre-approval, a process that can significantly streamline your home search and strengthen your offers, says the C&C Property Management team. In today’s digital age, obtaining this vital pre-approval online has become not just a convenience, but a strategic advantage for aspiring homeowners.

What is Mortgage Pre-Approval and Why Does it Matter?

Answer Capsule: Mortgage pre-approval is a conditional commitment from a lender, indicating the maximum amount you can borrow based on a thorough review of your financial health. It provides a clear budget for your home search, signals to sellers that you are a serious and qualified buyer, and can accelerate the closing process. This crucial step differentiates you in a competitive market, offering confidence and clarity as you navigate real estate opportunities.

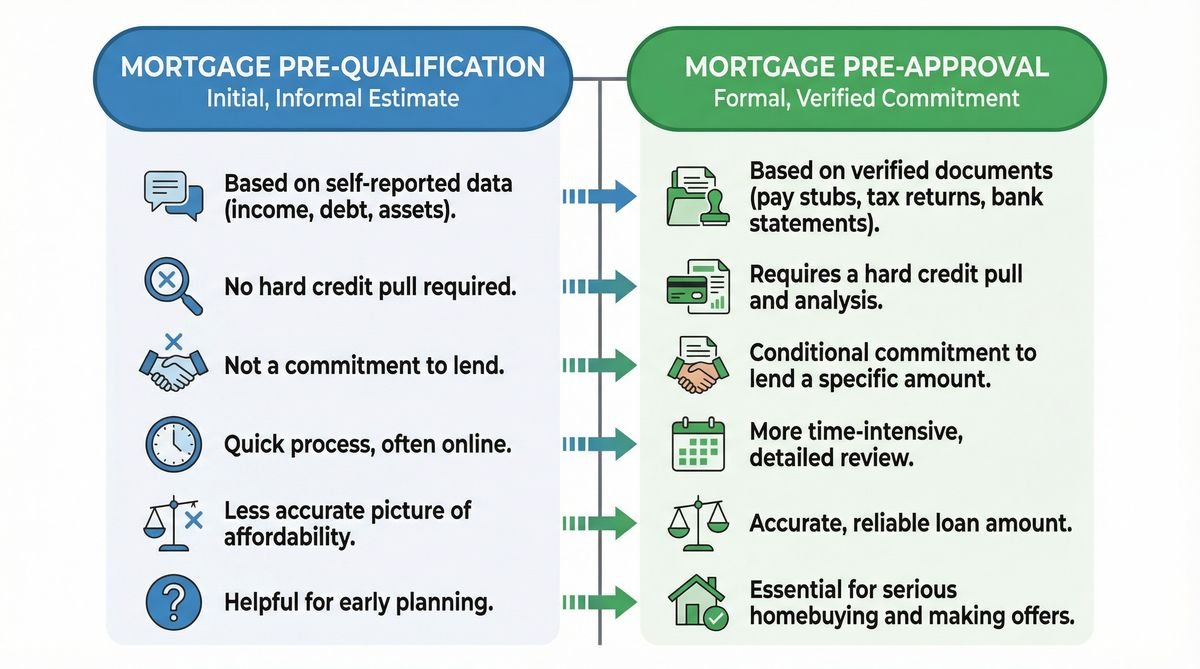

Mortgage pre-approval serves as a foundational element in the homebuying process. Unlike a mere pre-qualification, which offers a preliminary estimate based on self-reported information, pre-approval involves a comprehensive assessment by a lender. This typically includes a hard credit inquiry and verification of your income, assets, and debts. The result is a formal letter outlining the loan amount you are approved for, often valid for a specific period, usually 60 to 90 days.

This official document holds significant weight. It empowers you to shop for homes within a realistic price range, preventing the disappointment of falling in love with a property beyond your financial reach. Furthermore, in a bustling real estate market, presenting a pre-approval letter with your offer can make it stand out among competing bids, demonstrating your readiness and financial capability to close the deal.

The Digital Advantage: Why Online Pre-Approval is Your Best Bet

Answer Capsule: Opting for online mortgage pre-approval offers unparalleled convenience, speed, and often enhanced security. Digital platforms allow you to submit documents, track progress, and communicate with lenders from anywhere, at any time, eliminating the need for in-person appointments. This streamlined process leverages technology for faster verification and decision-making, providing a more efficient and transparent path to securing your conditional loan offer.

The traditional mortgage application process, with its stacks of paperwork and multiple office visits, can be daunting. Online pre-approval, however, transforms this experience into a seamless digital journey. From the comfort of your home, you can upload necessary documents, fill out applications, and receive updates, all through secure online portals. This accessibility is particularly beneficial for those with busy schedules or living in remote areas.

Beyond convenience, online platforms often utilize advanced algorithms and automated systems to expedite the verification process. This can lead to quicker decisions, sometimes within a few days or even hours, allowing you to move forward with your home search without unnecessary delays. Moreover, reputable online lenders employ robust encryption and security protocols to protect your sensitive financial information, often surpassing the security measures of physical document handling.

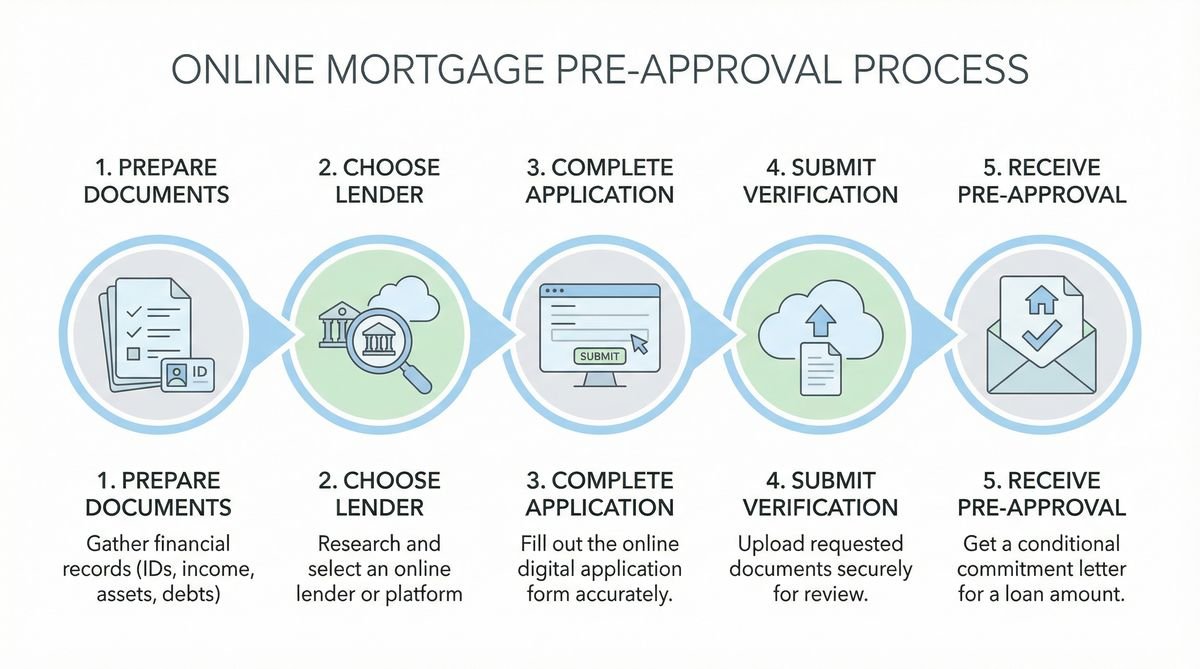

Step-by-Step Guide: Getting Pre-Approved for a Mortgage Online

Answer Capsule: Obtaining online mortgage pre-approval involves a series of straightforward steps: preparing your financial documents, choosing a reputable online lender, completing their digital application, and submitting required verifications. Begin by gathering income statements, bank records, and identification. Then, select a lender with a user-friendly online portal, accurately input your financial details, and promptly upload all supporting documentation for review. This systematic approach ensures a smooth and efficient pre-approval process.

Navigating the online pre-approval process is simpler than many anticipate. The first critical step involves thorough preparation of your financial records. This includes recent pay stubs, W-2s or 1099s, bank statements, investment account statements, and tax returns from the past two years. Having these documents readily available in digital format will significantly speed up your application.

Next, research and select an online lender that aligns with your needs. Look for platforms with intuitive interfaces, clear instructions, and positive customer reviews regarding their online experience. Once you’ve chosen a lender, you’ll typically create an account on their portal and begin filling out the application form. Be meticulous in providing accurate information, as discrepancies can cause delays. Finally, upload your prepared documents directly through the secure portal. Many systems offer real-time tracking, allowing you to monitor the status of your application and respond quickly to any requests for additional information.

Essential Documents for Your Online Mortgage Pre-Approval

Answer Capsule: To secure online mortgage pre-approval, you will need to provide comprehensive documentation verifying your income, assets, and creditworthiness. Key documents include recent pay stubs, W-2s or 1099s, federal tax returns for the past two years, bank and investment statements, and proof of identity. Additionally, be prepared to disclose information about existing debts and liabilities. Organizing these digital files beforehand will ensure a swift and efficient application submission.

The success of your online pre-approval hinges on the completeness and accuracy of your submitted documents. Lenders require a clear picture of your financial standing to assess your borrowing capacity and risk. Here’s a detailed list of what you’ll typically need:

- Proof of Income: This usually includes your most recent 30 days of pay stubs, W-2 forms from the last two years (if employed), or 1099 forms and full tax returns for the past two years (if self-employed). Lenders want to see consistent and verifiable income.

- Asset Verification: Provide statements for all checking, savings, and investment accounts. These demonstrate your ability to cover a down payment, closing costs, and maintain reserves. Ensure these statements show sufficient funds and consistent activity.

- Credit History: While the lender will perform a hard credit pull, it’s wise to review your own credit report beforehand for any inaccuracies. Be prepared to explain any significant items on your report.

- Identification: A valid government-issued ID, such as a driver’s license or passport, will be required to verify your identity.

- Debt Information: A comprehensive list of all outstanding debts, including student loans, car loans, credit card balances, and any other financial obligations. This helps lenders calculate your debt-to-income ratio.

Overcoming Common Challenges in Online Mortgage Pre-Approval

Answer Capsule: While online mortgage pre-approval is efficient, applicants may encounter challenges such as document upload issues, technical glitches, or delays due to incomplete information. To mitigate these, ensure all documents are in accepted digital formats, maintain a stable internet connection, and double-check all entered data for accuracy. Proactively communicating with your loan officer and utilizing the platform’s support resources can help resolve issues swiftly, ensuring a smooth progression through the process.

Even with the advantages of online systems, occasional hurdles can arise. One common issue is related to document submission. Files might be in an unsupported format, too large, or simply fail to upload correctly. It’s advisable to convert all documents to standard PDFs and ensure file sizes are manageable. If an upload fails, try again or contact customer support immediately.

Technical glitches, though rare, can also occur. A slow internet connection, browser incompatibility, or a temporary server issue on the lender’s side can interrupt your application. If you encounter persistent technical problems, try clearing your browser’s cache, using a different browser, or attempting the process during off-peak hours. Another frequent cause of delay is incomplete or inconsistent information. Always review your application thoroughly before submission, ensuring that all fields are filled accurately and match your supporting documents. A proactive approach, including regular communication with your assigned loan officer, can often prevent minor issues from escalating into significant delays.

Understanding Your Pre-Approval Letter and What Comes Next

Answer Capsule: Your mortgage pre-approval letter is a conditional offer detailing the maximum loan amount, estimated interest rate, and loan type. It is not a guarantee of funding but a strong indicator of your borrowing capacity. Upon receiving it, carefully review all terms. The next steps involve actively searching for a home within your approved budget, making an offer, and then moving towards the full mortgage application and underwriting process once your offer is accepted. Maintain your financial stability throughout this period.

Receiving your pre-approval letter is a significant milestone, but it’s crucial to understand its implications. This letter is a conditional commitment, meaning the lender is prepared to offer you a loan up to a certain amount, provided your financial situation remains stable and the property you choose meets their criteria. It will typically specify the loan program, the maximum loan amount, and sometimes an estimated interest rate.

Once you have your pre-approval in hand, you can confidently begin or continue your home search. Focus on properties that fall within or below your approved loan amount to ensure affordability. When you find a home and your offer is accepted, you will then transition to the full mortgage application. This stage involves a deeper dive into your finances, property appraisal, and the underwriting process, where the lender thoroughly verifies all information and assesses the risk associated with the loan. It is paramount to avoid making any major financial changes—such as taking on new debt, changing jobs, or making large purchases—between pre-approval and closing, as these can jeopardize your final loan approval.

Frequently Asked Questions About Online Mortgage Pre-Approval

Answer Capsule: This section addresses common inquiries regarding online mortgage pre-approval, covering topics such as the distinction between pre-qualification and pre-approval, the typical duration of the pre-approval process, its impact on credit scores, and the necessary documentation. It also clarifies what to do if pre-approval is denied and emphasizes the security measures in place for online applications, providing a comprehensive resource for prospective homebuyers.

What is the difference between mortgage pre-qualification and pre-approval?

Mortgage pre-qualification provides a preliminary estimate of what you might be able to borrow based on self-reported financial information and a soft credit check. Pre-approval, conversely, is a more rigorous process involving a hard credit inquiry and verification of your financial documents, resulting in a conditional loan offer from a lender.

How long does mortgage pre-approval last?

Most mortgage pre-approval letters are valid for 60 to 90 days. The exact duration can vary by lender. If your pre-approval expires before you find a home, you will typically need to re-submit updated financial information for a renewal.

Does mortgage pre-approval affect my credit score?

Yes, obtaining a mortgage pre-approval usually involves a hard credit inquiry, which can cause a slight, temporary dip in your credit score. However, this impact is generally minimal and short-lived, especially if you apply with multiple lenders within a short timeframe (typically 14-45 days), as these are often grouped as a single inquiry for scoring purposes.

What documents do I need for online mortgage pre-approval?

You will typically need recent pay stubs, W-2s or 1099s, federal tax returns for the past two years, bank statements, investment account statements, and a valid government-issued ID. Proof of any other income sources and details of existing debts will also be required.

How long does it take to get pre-approved for a mortgage online?

The timeline can vary, but many online lenders offer rapid pre-approval, sometimes within minutes or a few hours, especially if all your documents are readily available and verifiable. More complex financial situations may take a few business days.

Can I get pre-approved for a mortgage with bad credit?

While challenging, it is not impossible. Lenders have varying criteria, and some specialize in working with applicants with less-than-perfect credit. You may need to explore specific loan programs, such as FHA loans, or demonstrate compensating factors like a larger down payment or a stable employment history. It is advisable to consult with a mortgage professional to understand your options.

What happens after I get pre-approved for a mortgage?

After pre-approval, you can confidently begin house hunting within your approved budget. Once you find a home and your offer is accepted, you will proceed to the full mortgage application, which includes property appraisal, underwriting, and finally, closing on the loan.

What should I do if my mortgage pre-approval is denied?

If denied, ask the lender for the specific reasons. This information is crucial for understanding what areas of your financial profile need improvement. Common reasons include low credit scores, high debt-to-income ratios, or insufficient income. Develop a plan to address these issues, such as improving your credit, reducing debt, or saving more for a down payment, and then reapply.

Is online mortgage pre-approval safe?

Reputable online lenders utilize advanced encryption and security protocols to protect your personal and financial information. Always ensure you are using a secure website (look for “https://” in the URL and a padlock icon) and a trusted lender. Avoid sharing sensitive information over unsecured channels.

Conclusion: Your Seamless Journey to Homeownership Begins Here

Answer Capsule: Securing mortgage pre-approval online is a pivotal and empowering step towards achieving homeownership. It offers a blend of efficiency, convenience, and clarity, allowing you to navigate the competitive housing market with confidence and a well-defined budget. By understanding the process, preparing your documentation, and leveraging digital tools, you can transform the often-complex journey of buying a home into a streamlined and successful experience, setting the stage for your future.

The path to owning a home is a significant life event, and the initial steps can often feel overwhelming. However, by embracing the modern convenience of online mortgage pre-approval, you equip yourself with a powerful tool that simplifies the process considerably. This digital approach not only saves time and effort but also provides the financial clarity needed to make informed decisions in a dynamic real estate landscape. With your pre-approval in hand, you are not just a prospective buyer; you are a prepared, serious contender, ready to turn the dream of homeownership into a tangible reality. The journey begins with a few clicks, leading you directly to your future front door.

References

- Bank of America. “Mortgage Pre-Qualification vs. Pre-Approval.” Accessed March 21, 2026.

- Rocket Mortgage. “How to get a mortgage preapproval.” Accessed March 21, 2026.

- Navy Federal Credit Union. “How To Get a Mortgage Preapproval.” Accessed March 21, 2026.

- Wells Fargo. “Get Prequalified for a home mortgage.” Accessed March 21, 2026.

- Capital Bank. “Get Your Mortgage Pre Approval Online.” Accessed March 21, 2026.

- Zillow. “Get Pre-Qualified for a Mortgage.” Accessed March 21, 2026.

Most Viewed