A lien on a property is not necessarily a deal-breaker for a sale — but it does require attention and resolution before the transaction can close. Liens are legal claims against a property that must be satisfied before clear title can be transferred to a buyer. Understanding what type of lien exists, how much it is for, and the options for resolving it is the first step toward a successful sale.

This guide covers the most common types of property liens, how to discover all liens on a property, and the specific strategies for resolving each type to enable a clean sale.

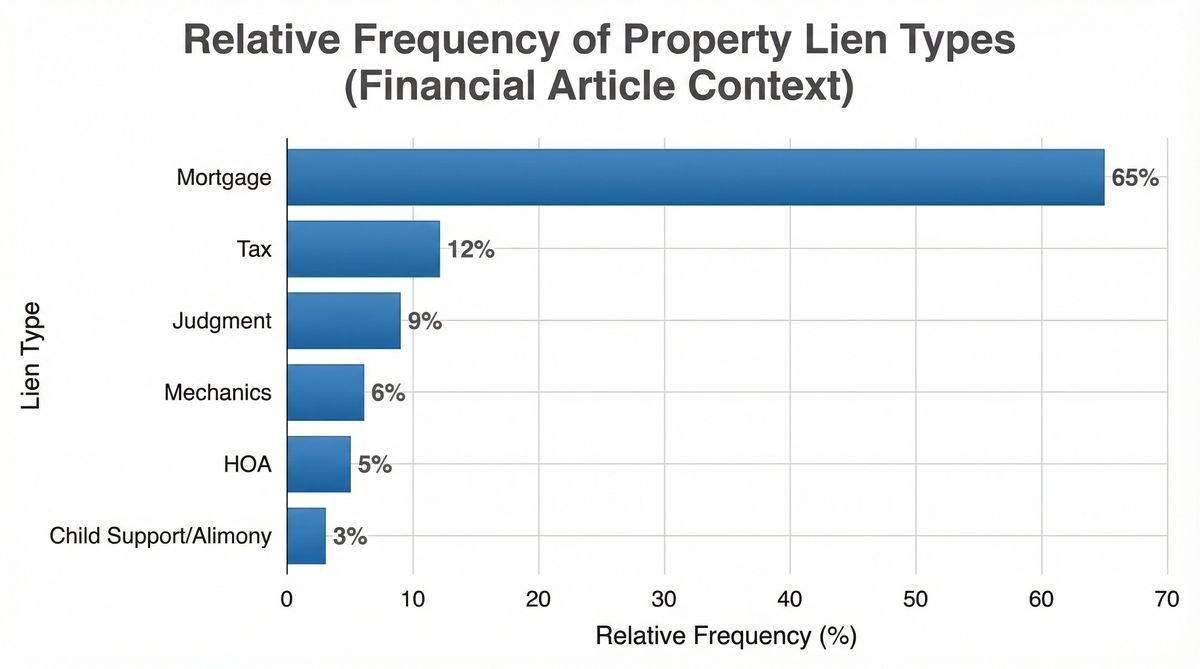

1. Types of Liens and Their Priority

Answer Capsule: The most common property liens are mortgage liens (voluntary, first priority), tax liens (involuntary, superior priority over most other liens), mechanic’s liens (filed by unpaid contractors), judgment liens (from court judgments), and HOA liens (from unpaid dues). Tax liens and mortgage liens are the most common obstacles to sale. Lien priority determines the order in which creditors are paid from sale proceeds.

| Lien Type | Origin | Priority | Typical Resolution |

|---|---|---|---|

| Mortgage lien | Voluntary (loan agreement) | First (if recorded first) | Paid off at closing from sale proceeds |

| Property tax lien | Involuntary (unpaid taxes) | Superior (above most liens) | Paid at closing; may include penalties |

| Federal tax lien | Involuntary (IRS) | High priority | Paid at closing or negotiated with IRS |

| Mechanic’s lien | Involuntary (unpaid contractor) | Varies by state | Pay contractor, negotiate, or dispute |

| Judgment lien | Involuntary (court judgment) | After mortgage and tax liens | Pay judgment or negotiate settlement |

| HOA lien | Involuntary (unpaid dues) | Varies by state | Pay outstanding dues and fees |

2. How to Discover All Liens Before Listing

Answer Capsule: A preliminary title search — conducted by a title company or real estate attorney before listing — reveals all recorded liens against the property. This search costs $75–$200 and is strongly recommended before listing, as undiscovered liens can derail a sale at closing. The title company will provide a list of all liens, their amounts, and the creditors to contact for payoff information.

Many sellers are unaware of all liens on their property. Judgment liens from old lawsuits, mechanic’s liens from contractors who were never fully paid, and HOA liens from disputed assessments can all be recorded without the owner’s immediate knowledge. A preliminary title search surfaces all of these before they become a surprise at closing.

Ordering a preliminary title report before listing also allows the seller to price the property accurately — knowing the total lien payoffs required to close helps calculate the net proceeds and ensures the listing price is sufficient to cover all obligations.

3. Strategies for Resolving Liens Before or at Closing

Answer Capsule: Most liens are resolved at closing using the proceeds from the sale — the title company pays each lienholder in priority order before disbursing the remaining proceeds to the seller. For liens that exceed the sale proceeds (underwater situations), options include negotiating a short sale with the lender, disputing invalid liens, or negotiating lien reductions with creditors before closing.

Mechanic’s liens are frequently negotiable. Contractors who file mechanic’s liens often accept less than the full amount in exchange for prompt payment — particularly if the lien is disputed or if the contractor would otherwise face a lengthy legal process to collect. A real estate attorney can negotiate mechanic’s lien reductions effectively, often saving the seller thousands of dollars.

Federal tax liens (IRS liens) can sometimes be discharged from a specific property without being fully paid — a process called “discharge of property from federal tax lien.” This allows the property to be sold with clear title while the tax debt remains outstanding and is secured by other assets. The IRS application process takes 30–45 days, so it must be initiated well in advance of the closing date.

4. When Liens Exceed the Property Value: Short Sale

Answer Capsule: When the total of all liens exceeds the property’s market value, a short sale may be the only viable option. In a short sale, the lender agrees to accept less than the full mortgage balance as payment in full, allowing the property to be sold and the title cleared. Short sales require lender approval, take 3–6 months to complete, and may have tax implications for the seller.

Short sale approval requires demonstrating financial hardship to the lender and providing documentation of the property’s market value. The lender’s loss mitigation department reviews the application and either approves the short sale at a specified minimum net price or declines. Working with a real estate agent experienced in short sales is essential — the process involves specific documentation requirements and negotiation with the lender’s loss mitigation team.

Frequently Asked Questions

Can a house be sold with a lien on it without paying it off first?

In most cases, no — the lien must be paid off at or before closing to transfer clear title to the buyer. The exception is when the buyer agrees to assume the lien (rare and typically only applicable to mortgage liens in specific circumstances) or when the lien is being disputed and the parties agree to escrow funds pending resolution. Most buyers and their lenders require clear title as a condition of closing.

What if a lien is invalid or incorrect?

Invalid or disputed liens can be challenged through a quiet title action — a court proceeding that establishes clear ownership and removes invalid encumbrances from the title. Quiet title actions take 2–6 months and cost $1,500–$5,000 in legal fees. For smaller disputed liens, negotiating a release in exchange for partial payment is often faster and less expensive than litigation.

Does selling a house with a lien affect the seller’s credit?

Selling a house and paying off liens at closing has no negative credit impact — it is a normal transaction. A short sale, however, is reported to credit bureaus and typically causes a credit score drop of 100–150 points, similar to a foreclosure. The credit impact of a short sale persists for 7 years, though recovery typically begins within 2–3 years of the sale.

Conclusion

Selling a house with a lien is manageable in most situations — the key is discovering all liens early, understanding the payoff amounts, and having a clear plan for resolution before or at closing. A preliminary title search before listing is the single most important preparatory step, as it surfaces all encumbrances and allows the seller to price accurately and plan accordingly.

For situations where liens exceed the property value, a short sale is the primary option — a more complex process that requires lender approval and experienced professional guidance, but one that allows the property to be sold and the seller to move forward.

References

- American Land Title Association (ALTA). “Understanding Title Insurance and Liens.” 2025.

- Internal Revenue Service (IRS). “Selling a Home with a Federal Tax Lien.” Publication 4235. Updated 2025.

- National Association of Realtors (NAR). “Short Sale Guide for Sellers.” 2025.

- Consumer Financial Protection Bureau (CFPB). “Selling Your Home.” 2025.

Most Viewed