Imagine finding your dream home, but a less-than-perfect credit score or a modest down payment stands in your way. For many aspiring homeowners, this scenario is a common hurdle. However, a lease option can offer a unique pathway to bridge this gap, allowing you to move into your desired property now with the potential to purchase it later. This article will demystify lease options, explaining how they work, their benefits, and the crucial considerations for buyers.

What is a Lease Option?

Answer Capsule: A lease option is a real estate agreement that grants a tenant the right, but not the obligation, to purchase a rented property at a predetermined price within a specified timeframe. It combines a standard rental agreement with an option contract, providing flexibility for buyers who need time to prepare for homeownership while securing a future purchase price.

A lease option, often referred to as a rent-to-own agreement, is a unique arrangement that blends renting with the potential for future ownership. It essentially consists of two interconnected contracts: a standard residential lease and an option to purchase. This structure allows you to occupy the property as a tenant while holding the exclusive right to buy it before the lease term expires.

The core appeal of a lease option lies in its flexibility. Unlike a traditional purchase, you are not immediately committing to a mortgage. Instead, you are buying time. This time can be invaluable for improving your credit score, saving for a larger down payment, or simply test-driving the neighborhood before making a long-term commitment. The property owner benefits from a steady rental income and a potential future sale, often at a premium price.

Lease Option vs. Lease Purchase: Understanding the Key Differences

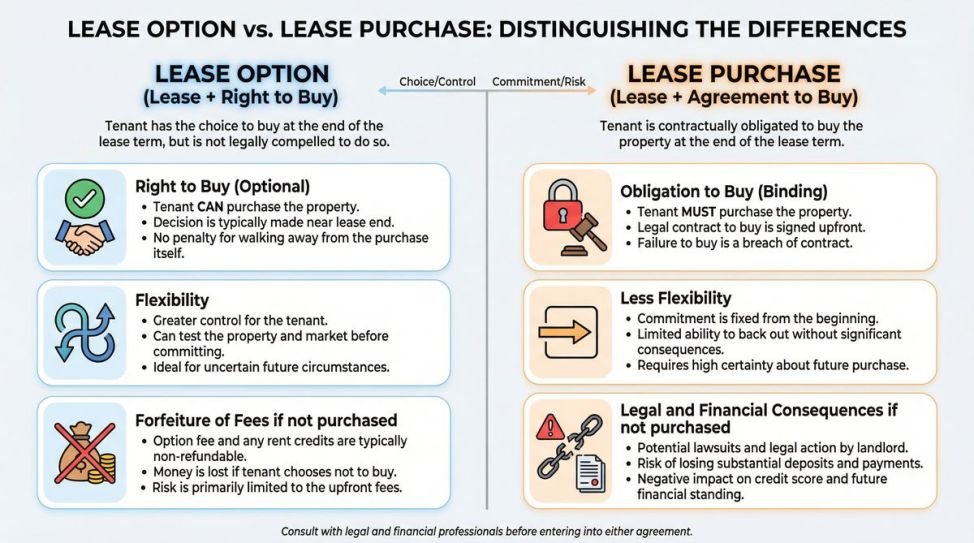

Answer Capsule: The primary difference lies in obligation. A lease option gives the buyer the choice to purchase the property at the end of the lease, whereas a lease purchase legally obligates the buyer to complete the transaction. A lease option offers flexibility to walk away, while a lease purchase is a binding commitment to buy.

While often used interchangeably, lease options and lease purchases are distinct legal agreements with significantly different implications for the buyer. Understanding this distinction is crucial before signing any rent-to-own contract. A lease option provides a safety net. If your financial situation does not improve as expected, or if you decide the home is not the right fit, you can simply walk away at the end of the lease term. Your only loss is the upfront option fee and any rent premiums paid.

Conversely, a lease purchase is a firm commitment. When you sign a lease purchase agreement, you are legally bound to buy the property at the end of the lease, regardless of your financial readiness or changes in the housing market. Failing to secure financing or complete the purchase can result in severe legal and financial consequences, including breach of contract lawsuits. Therefore, a lease option is generally considered the safer and more flexible route for aspiring homeowners.

How Does a Lease Option Work for Buyers? A Step-by-Step Guide

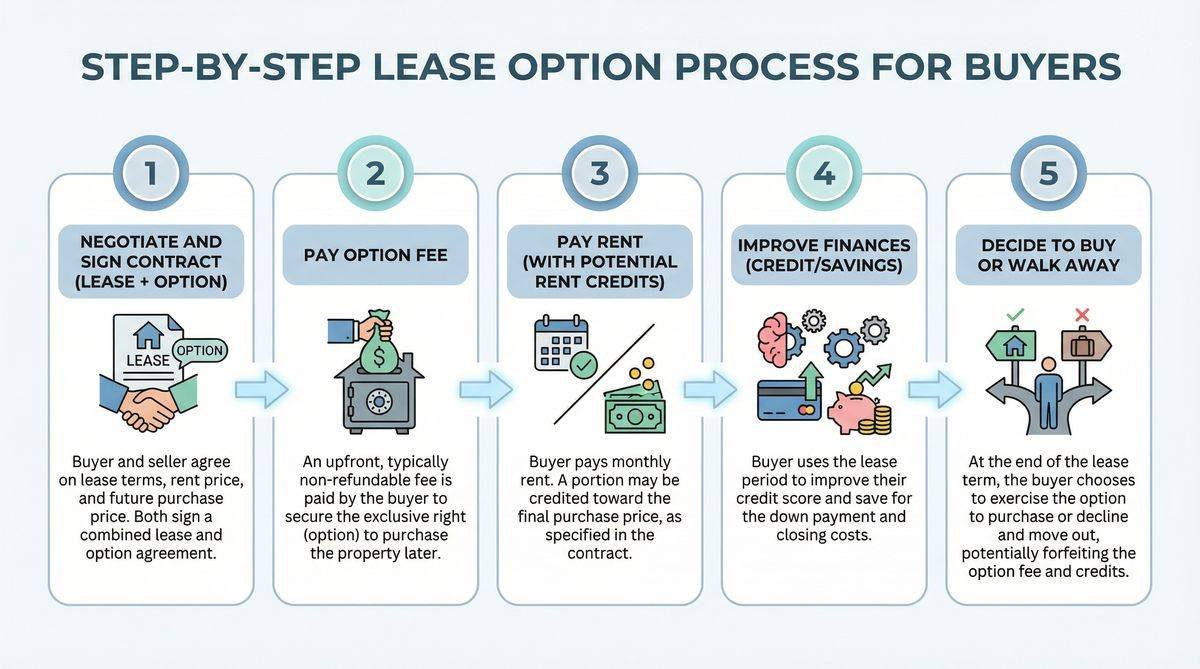

Answer Capsule: The process involves negotiating terms, paying an upfront non-refundable option fee, and signing the agreement. You then pay monthly rent, often with a premium credited toward the future purchase. Before the lease ends, you must secure financing and exercise your option to buy, or choose to walk away.

Entering a lease option agreement involves several distinct steps, each requiring careful consideration and negotiation. The process begins with finding a willing seller and agreeing on the fundamental terms. This includes the future purchase price, the duration of the lease (typically one to three years), and the amount of the option fee. The option fee is a non-refundable upfront payment, usually ranging from 1% to 5% of the purchase price, which secures your exclusive right to buy the property.

Once the terms are set, you will sign the combined lease and option contracts. During the lease period, you will pay monthly rent. In many lease option agreements, a portion of this rent, known as a rent credit or premium, is set aside and applied toward your eventual down payment. This premium is typically above the standard market rent for the area. As the end of the lease term approaches, you must decide whether to exercise your option. If you choose to buy, you will need to secure a traditional mortgage to complete the purchase. If you decide not to buy, the option expires, and you forfeit the option fee and any accumulated rent credits.

Benefits of a Lease Option for Aspiring Homeowners

Answer Capsule: Lease options offer buyers the ability to lock in a purchase price, build equity through rent credits, and test-drive a home before committing. They provide crucial time to improve credit scores and save for a down payment while living in the desired property, making homeownership accessible to those currently unable to secure traditional financing.

For buyers facing temporary financial hurdles, a lease option presents several compelling advantages. One of the most significant benefits is the ability to lock in a purchase price upfront. In an appreciating housing market, this can be highly advantageous. Even if the property’s value increases significantly during your lease term, you are only obligated to pay the price agreed upon at the beginning of the contract. This protects you from being priced out of the market while you prepare for homeownership.

Furthermore, lease options allow you to build equity, or at least a down payment fund, while renting. The rent credits accumulated over the lease term can significantly reduce the amount you need to borrow when it comes time to purchase. Additionally, living in the home before buying provides a unique opportunity to test-drive the property and the neighborhood. You can uncover any hidden issues with the house or decide if the community truly fits your lifestyle before making a permanent commitment.

Navigating the Risks: What Buyers Need to Know About Lease Options

Answer Capsule: Key risks include losing the non-refundable option fee and rent credits if you choose not to buy or cannot secure financing. Buyers also face the risk of market depreciation, where the locked-in price exceeds the home’s current value, and potential complexities regarding maintenance responsibilities during the lease period.

While lease options offer a pathway to homeownership, they are not without significant risks. The most prominent risk is the potential loss of your financial investment. If you decide not to purchase the home at the end of the lease, or if you are unable to secure a mortgage, you will forfeit the upfront option fee and all accumulated rent credits. This can amount to a substantial sum of money lost without gaining any equity in the property.

Another critical risk involves market fluctuations. While locking in a purchase price protects you in an appreciating market, it can be detrimental if property values decline. If the home’s market value falls below your agreed-upon purchase price, you may find yourself overpaying for the property or struggling to secure a mortgage for more than the home is worth. Additionally, lease option agreements often place the burden of maintenance and repairs on the tenant, which can lead to unexpected expenses during the rental period.

Who Benefits Most from a Lease Option? Buyer Profiles Explored

Answer Capsule: Lease options are ideal for buyers who need 12 to 36 months to improve their credit scores, save for a larger down payment, or establish a consistent employment history. They also suit individuals relocating to a new area who want to test a neighborhood before committing to a purchase.

Lease options are not a one-size-fits-all solution, but they are particularly well-suited for specific buyer profiles. The most common candidate is someone with a steady income but a less-than-ideal credit score. A lease option provides the necessary runway—typically one to three years—to pay down debt, resolve credit issues, and improve their score to qualify for a favorable mortgage rate. This period allows them to transition from a risky borrower to a prime candidate for traditional financing.

Another group that benefits significantly includes those who lack a substantial down payment. By utilizing rent credits, buyers can systematically build their down payment over time, making the final purchase more manageable. Furthermore, individuals who are self-employed or have recently changed careers may use a lease option to establish the consistent employment history that lenders require. Finally, buyers relocating to an unfamiliar area can use a lease option to ensure the community and the specific home meet their long-term needs before finalizing a purchase.

Lease Option FAQs for Buyers

What is an option fee in a lease option?

An option fee is a non-refundable upfront payment made by the tenant to the property owner. This fee secures the tenant’s exclusive right to purchase the property at a predetermined price within a specified timeframe. It typically ranges from 1% to 5% of the agreed-upon purchase price and is often credited toward the down payment if the tenant exercises the option to buy.

Does a lease option help build credit?

A lease option itself does not automatically build credit, as rent payments are not typically reported to credit bureaus. However, you can request that your landlord report your on-time rent payments to the major credit bureaus, which can help improve your score. The primary way a lease option aids credit building is by providing the time needed to actively manage and improve your financial profile before applying for a mortgage.

Can I get out of a lease option agreement?

Yes, you can get out of a lease option agreement by simply choosing not to exercise your option to buy at the end of the lease term. Because it is an option and not an obligation, you are free to walk away. However, doing so means you will forfeit the non-refundable option fee and any rent premiums you paid toward the purchase price during the lease period.

Conclusion: Is a Lease Option Right for Your Homeownership Journey?

A lease option can be a powerful tool for aspiring homeowners who need a little more time to get their financial house in order. By offering the chance to lock in a purchase price, build a down payment through rent credits, and test-drive a property, it provides a flexible bridge between renting and owning. However, the risks are real. The potential loss of upfront fees and rent credits, coupled with the uncertainties of the housing market and financing approval, means this path requires careful consideration and diligent financial planning.

Before entering a lease option agreement, it is crucial to assess your long-term financial goals and your ability to secure a mortgage within the lease timeframe. Consulting with a real estate attorney and a financial advisor can help you navigate the complexities of the contract and ensure the terms are fair and achievable. Ultimately, a lease option is not a shortcut to homeownership, but rather a structured, time-bound opportunity to prepare for it.

References

- Chase. “Lease Option: Definition, How It Works, Pros & Cons.”

- National Association of REALTORS®. “Lease-Option Purchases.”

- Rocket Mortgage. “Lease option: Definition and how it works.”

Most Viewed