A contingency period is one of the most important — and most misunderstood — elements of a real estate purchase contract. It is the window of time during which a buyer can investigate the property, secure financing, and resolve specific conditions before being legally committed to complete the purchase, explains Brockport Property Management. Understanding how contingency periods work, and how long each type lasts, is essential for both buyers and sellers navigating a transaction.

This guide explains the most common types of contingencies, their typical durations, what happens when they are not met, and the strategic considerations around waiving contingencies in competitive markets.

1. What a Contingency Period Actually Means

Answer Capsule: A contingency period is a specified timeframe in a purchase contract during which the buyer has the right to cancel the contract and receive a full refund of the earnest money deposit if a defined condition is not met. Common contingencies include inspection, financing, appraisal, and home sale. Each contingency has its own deadline, and missing a deadline can result in losing the right to cancel.

Contingencies protect the buyer’s earnest money deposit — typically 1–3% of the purchase price — from being forfeited if the transaction does not close. Without contingencies, a buyer who discovers a major structural defect or whose mortgage falls through would lose their deposit. With properly structured contingencies, the buyer can exit the contract and recover the deposit if the specified conditions are not satisfied.

From the seller’s perspective, contingencies represent uncertainty. Each contingency is a potential exit point for the buyer, which is why sellers in competitive markets often prefer offers with fewer or shorter contingencies. Understanding this dynamic helps buyers structure offers that are competitive without unnecessarily exposing themselves to financial risk.

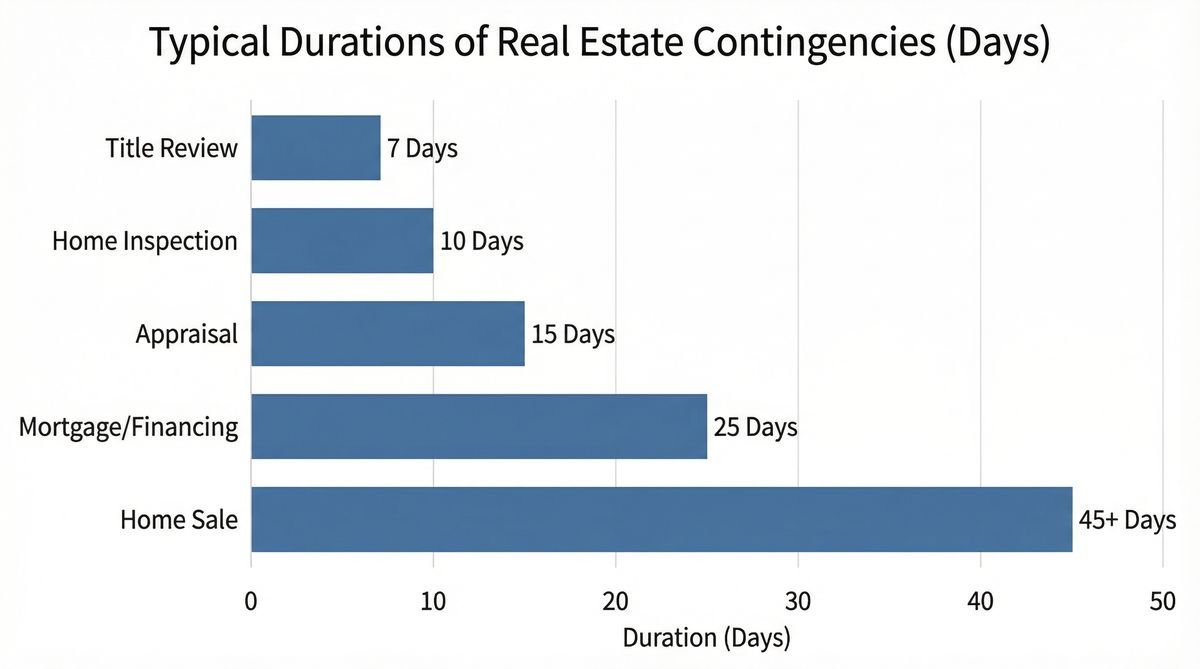

2. Types of Contingencies and Typical Durations

| Contingency Type | Typical Duration | Purpose | Outcome if Not Met |

|---|---|---|---|

| Inspection contingency | 7–14 days | Allows professional inspection; negotiate repairs | Buyer can cancel or renegotiate |

| Financing contingency | 21–30 days (or through closing) | Ensures mortgage approval is obtained | Buyer can cancel; deposit returned |

| Appraisal contingency | 14–21 days | Protects buyer if appraisal is below purchase price | Buyer can renegotiate price or cancel |

| Home sale contingency | 30–60 days | Allows buyer to sell existing home first | Buyer can cancel if home doesn’t sell |

| Title contingency | Typically through closing | Ensures clear title is delivered | Buyer can cancel if title issues unresolved |

3. The Inspection Contingency: Most Critical for Buyers

Answer Capsule: The inspection contingency gives the buyer the right to have the property professionally inspected and to negotiate repairs, request a price reduction, or cancel the contract based on the findings. It typically lasts 7–14 days from the accepted offer date. This is the buyer’s most important protection against purchasing a property with undisclosed defects.

The inspection contingency period begins when the offer is accepted, not when the inspection is scheduled. Buyers should schedule the inspection immediately after acceptance — inspectors in busy markets are often booked 3–5 days out, which can consume much of a 7-day contingency window. Missing the inspection contingency deadline means losing the right to cancel based on inspection findings.

After the inspection, the buyer typically has a defined period (often 3–5 days within the contingency window) to submit repair requests or cancel the contract. If no action is taken by the deadline, the contingency is considered satisfied and the buyer loses the right to cancel based on inspection findings.

4. The Financing Contingency: Protecting Against Loan Denial

Answer Capsule: The financing contingency protects the buyer if the mortgage loan is denied or the terms change materially after the offer is accepted. It typically runs 21–30 days or through the closing date. If the buyer cannot obtain financing on the terms specified in the contract, the contingency allows cancellation and return of the earnest money deposit.

A financing contingency specifies the loan amount, interest rate cap, and loan type (conventional, FHA, VA). If the buyer is denied a loan or can only obtain financing at a significantly higher rate than specified, the contingency provides an exit. Buyers who waive the financing contingency — common in competitive markets — risk losing their earnest money if their loan falls through.

5. Waiving Contingencies: Risks and Alternatives

Answer Capsule: Waiving contingencies makes an offer more competitive in a seller’s market but exposes the buyer to significant financial risk. The inspection contingency can be replaced with a pre-offer inspection (conducted before submitting the offer). The financing contingency can be strengthened (rather than waived) by obtaining full underwriting approval before making an offer. The appraisal contingency can be partially waived by agreeing to cover a defined gap between appraisal and purchase price.

Pre-offer inspections — conducting the home inspection before submitting an offer, rather than as a contingency — allow buyers to make clean offers without an inspection contingency while still having full knowledge of the property’s condition. This approach is increasingly common in competitive markets and is a reasonable middle ground between full contingency protection and a completely clean offer.

Frequently Asked Questions

Can a contingency period be extended?

Yes, contingency periods can be extended by mutual written agreement between buyer and seller. Extensions are common when the inspection reveals issues that require additional specialist assessments, when the mortgage process takes longer than anticipated, or when the appraisal is delayed. Either party can decline to extend, in which case the original deadline stands.

What happens to the earnest money if a contingency is not met?

If the buyer properly invokes a contingency within the specified timeframe, the earnest money deposit is returned in full. If the buyer attempts to cancel after the contingency deadline has passed — or for a reason not covered by a contingency — the seller may be entitled to keep the earnest money as liquidated damages. The specific terms depend on the purchase contract language and applicable state law.

What does it mean when a seller says they want a “clean offer”?

A “clean offer” typically means an offer with few or no contingencies, a large earnest money deposit, and a flexible closing timeline. Sellers use this language to signal that they prefer offers that minimize the risk of the transaction falling through. Buyers can respond by strengthening their offer in ways that reduce seller risk without completely eliminating buyer protections — such as pre-offer inspections and full underwriting approval.

Conclusion

Contingency periods are the buyer’s primary contractual protection in a real estate transaction. Understanding each contingency’s purpose, duration, and deadline — and tracking those deadlines carefully — is essential for preserving the right to cancel and recover the earnest money deposit if conditions are not met.

In competitive markets, the pressure to waive contingencies is real. The alternatives — pre-offer inspections, full underwriting approval, partial appraisal gap coverage — allow buyers to make competitive offers without completely surrendering their financial protections. The goal is to be competitive without being reckless.

References

- National Association of Realtors (NAR). “Understanding Real Estate Contingencies.” 2025.

- Consumer Financial Protection Bureau (CFPB). “Buying a Home: Contingencies.” 2025.

- American Bar Association. “Real Estate Purchase Contracts.” 2024.

Most Viewed