Buying a foreclosure property with no money down is possible — but it requires combining the right loan program with the right type of foreclosure property, explains the TJC Real Estate Westminster team. The path is narrower than most real estate content suggests, and understanding the specific requirements upfront prevents wasted time pursuing strategies that do not apply to a particular buyer’s situation.

This guide covers the legitimate no-money-down loan programs that can be used to purchase foreclosure properties, the types of foreclosures each program applies to, and the practical realities of the process that most guides gloss over.

1. No-Money-Down Loan Programs for Foreclosures

Answer Capsule: The three primary no-money-down loan programs applicable to foreclosure purchases are VA loans (for eligible veterans and active military), USDA loans (for rural and suburban properties meeting income and location requirements), and FHA loans with down payment assistance programs. Standard FHA loans require 3.5% down — but paired with state or local down payment assistance grants, the effective out-of-pocket cost can be zero.

| Program | Down Payment | Eligibility | Property Requirements |

|---|---|---|---|

| VA Loan | 0% | Veterans, active military, surviving spouses | Must meet VA minimum property requirements (MPR) |

| USDA Loan | 0% | Income limits; rural/suburban location | Must be in USDA-eligible area; must meet condition standards |

| FHA + Down Payment Assistance | 0% effective | Income limits vary by program | Must meet FHA minimum property standards (MPS) |

| HUD Good Neighbor Next Door | 50% discount + FHA financing | Teachers, firefighters, EMTs, law enforcement | HUD-owned properties in revitalization areas only |

2. The Biggest Challenge: Property Condition Requirements

Answer Capsule: The most significant obstacle to buying a foreclosure with no money down is property condition. VA, USDA, and FHA loans all require the property to meet minimum condition standards — and foreclosure properties are frequently in poor condition. Structural damage, non-functional systems, safety hazards, and deferred maintenance can disqualify a foreclosure from government-backed financing, leaving only conventional loans (which require down payments) as an option.

FHA Minimum Property Standards (MPS) require that the home be safe, sound, and secure. Specific disqualifying conditions include: missing or non-functional HVAC systems, roof damage with active leaks, exposed electrical wiring, broken windows, evidence of active pest infestation, and structural damage. A foreclosure that has been vacant for an extended period often has multiple MPS violations.

The FHA 203(k) rehabilitation loan is specifically designed to address this problem. It combines the purchase price and renovation costs into a single loan, allowing buyers to purchase a distressed foreclosure and finance the repairs needed to bring it up to FHA standards. The 203(k) requires a minimum 3.5% down payment — but paired with down payment assistance, it can be an effective zero-down path to a foreclosure purchase.

3. Types of Foreclosures and Which Are Accessible

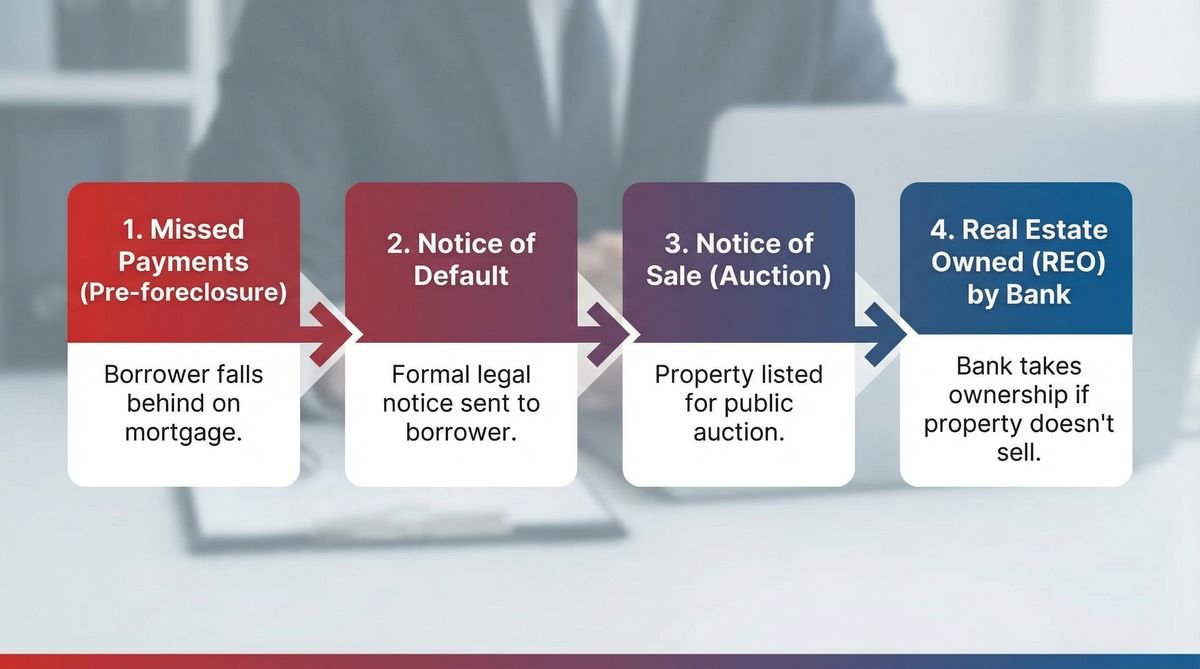

Answer Capsule: HUD-owned homes (foreclosures on FHA-insured loans) are the most accessible foreclosure type for no-money-down buyers because they are specifically listed for owner-occupant buyers and accept FHA financing. Bank-owned REO (Real Estate Owned) properties are sold by lenders and can be purchased with VA or USDA loans if they meet condition requirements. Courthouse auction foreclosures typically require cash and are not accessible with government-backed financing.

HUD homes are listed on HUDHomeStore.gov and are offered exclusively to owner-occupant buyers for the first 30 days before investors can bid. This exclusive window gives primary-residence buyers a significant advantage. HUD homes are sold as-is, but HUD provides a property condition report and allows inspections before bidding.

Bank-owned REO properties are listed through standard MLS channels and real estate agents. They can be purchased with VA or USDA financing if the property meets the respective program’s condition requirements. Many lenders will negotiate repairs or price reductions to make the property eligible for government-backed financing — it is worth asking.

4. Step-by-Step Process for a No-Money-Down Foreclosure Purchase

Answer Capsule: The process begins with loan pre-approval (VA, USDA, or FHA with DPA), followed by identifying eligible foreclosure properties through HUDHomeStore.gov or MLS listings, conducting a thorough inspection before making an offer, submitting an offer through a HUD-registered agent (for HUD homes), and navigating the longer closing timeline typical of government-backed foreclosure purchases (45–60 days).

Working with a real estate agent experienced in foreclosure purchases and government-backed loans is essential. HUD homes require a HUD-registered agent to submit bids. VA and USDA purchases require lenders experienced with those specific programs. The combination of a distressed property and a government loan program creates enough complexity that experienced professionals meaningfully improve the odds of a successful transaction.

Frequently Asked Questions

What is the HUD Good Neighbor Next Door program?

The HUD Good Neighbor Next Door (GNND) program offers eligible buyers — teachers, firefighters, emergency medical technicians, and law enforcement officers — a 50% discount on the list price of HUD-owned homes in designated revitalization areas. Buyers must commit to living in the property as their primary residence for at least 36 months. The program can be combined with FHA financing, making it one of the most powerful no-money-down options available for eligible buyers.

Can foreclosure auctions be purchased with no money down?

No. Courthouse auction foreclosures (pre-foreclosure auctions) require cash payment, typically within 24–48 hours of the auction. There is no financing contingency, no inspection period, and no title insurance in most auction purchases. These properties are inaccessible to buyers using government-backed financing and are generally appropriate only for experienced investors with cash reserves.

How long does it take to buy a foreclosure with no money down?

The timeline for a HUD home or REO purchase with government-backed financing is typically 45–75 days from accepted offer to closing — longer than a standard purchase due to additional appraisal requirements, condition inspections, and lender processing for government-backed loans. Buyers should account for this timeline when planning their move and avoiding lease expiration conflicts.

Conclusion

Buying a foreclosure with no money down is achievable for eligible buyers who understand the intersection of loan program requirements and foreclosure property types. VA loans for veterans, USDA loans for rural properties, and FHA financing with down payment assistance are the primary paths — each with specific eligibility requirements and property condition standards that must be met.

The property condition challenge is the most significant practical obstacle. HUD homes and bank-owned REO properties in reasonable condition are the most accessible targets. The FHA 203(k) rehabilitation loan expands the universe of eligible properties to include distressed foreclosures that need renovation — making it the most versatile tool for buyers committed to the no-money-down foreclosure strategy.

References

- U.S. Department of Housing and Urban Development (HUD). “Buying a HUD Home.” HUDHomeStore.gov. Updated 2025.

- U.S. Department of Veterans Affairs. “VA Home Loan Guaranty Program.” Updated 2025.

- USDA Rural Development. “Single Family Housing Guaranteed Loan Program.” Updated 2025.

- Consumer Financial Protection Bureau (CFPB). “Buying a Foreclosed Home.” 2025.

Most Viewed